How long do you need to recover the loss of real value in your equity portfolio?

This is a picture about the destruction of American savings, the difficulty and timing pertaining to the recovery of those values, and the punitive impact that taxes impose on that process.

This is likely your story if you had any investment in equities via:

- savings for your retirement, or

- your kids' educations or

- eldercare,

- a pension, SEP, Roth or regular IRA; or

- are a business or institutional portfolio manager or

- if you simply own a house (the numbers change a bit, but it’s generally the same story)

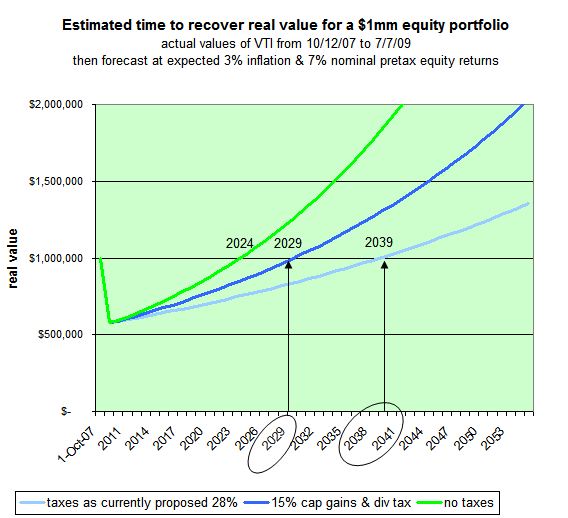

You likely won’t recover the real value of the portfolio value until 2039 and that seems to be a reasonably favorable scenario. It is clear that the increases of long term capital gains and dividend income taxes as proposed by the administration won't be helpful. Of course, if income and capital gains taxes are eliminated, it shortens the recovery from 2039 to about 2024. You can make your own call on that one.

The chart shows the decline of VTI, Vanguard's Total Stock Market Index ETF, from peak value on $78.26 on October 12, 2007 to $45.32 on July 7, 2009. VTI basically represents the entire US stock market, and the peak to trough decline you see is real. Thereafter, we assume a 7% nominal, pre-tax return on US equities. We may have over or under estimated future returns, but many managers would have been happy with 7% for the last few years and perhaps would be for the next few as well. We stipulate the forecast is primitive, but people can see and understand it. Monte Carlo simulation would be better, but it's harder to understand, and the zip code of the results won't change.

We assume a series of 366 day holding periods to simplify taxes. We also assume our initial basis to equal the proceeds of our first periodic sale, so all subsequent long term capital gains are taxed at the proposed federal rate of 28%. Dividends are taxed at the 28% proposed federal tax rate, and we added a 6% state income tax for the home team.

Play around with the assumptions if you like, but it won’t change fundamental and very sobering nature of the out outcomes: we’ve sacrificed the savings of several generations. In a steady state scenario, anyone over the age of about 27- 28 will likely run out of time and earnings capacity to catch up.

"So? I already knew I had a problem." Ok, in our next posting we'll talk about what this means for investment (and life) strategy going forward.

Assumptions:

2.64% dividend yield (ticker: VTI)

4.36% + expected price appreciation

7.00% = expected nominal pre tax equity return

0.90% less income tax on dividend

1.22% less LT cap gain (366 day holds)

4.88% = after tax equity return

3.00% less inflation

1.88% = real after tax equity return

3% inflation

34% fed dividend income tax as proposed at 28%+ 6% state

28% fed LT capital gains taxes proposed, no state

hb

hb

Reader Comments (2)

Hope everyone has a nice day!!!!!

What do you recommend for your clients approaching retirement age to preserve, in real terms, the existing value of their portfolios from taxes and inflation?