No mas! I’ll take #1, Monty!

"Every normal man must be tempted, at times, to spit on his hands, hoist the black flag, and begin slitting throats." — H.L. Mencken (Prejudices: First Series)

We have arrived. We encourage other citizens and investors to arrive as well. We call for no increase whatsoever in the federal debt limit. We call for scheduled real reductions in the aggregate consumption by state, local, and federal government of GDP. We believe that we are nearing the point where time is of the essence and further believe in the necessity of enlisting the discipline of the capital markets to achieve that objective. If the political circumstances require a technical or substantive default to invoke the discipline of the capital markets, so be it.

No more kicking the country’s can down the road. Fix it now. This posting has been simmering for a while, and the catalyst for publication, perhaps prematurely so, was Larry Summer’s article in the June 13th edition of the Financial Times, How We Can Avoid Stumbling Into Our Own Lost Decade. His thesis, reductively put, is an infinite do-loop, that the US suffers from lack of demand and further government spending will stimulate demand. For example, we should “take advantage of a moment when 10 year rates are below 3 per cent and construction employment approaches twenty per cent to expand infrastructure investment.” QED

Of course, there is never the question of what makes the economy actually work. The possibility of private investment, private labor is never even given consideration of any sort, nor any consideration given to the obstruction by government of the proper functioning markets or the loss of productivity. Just more government spending, more government debt, more distortion of the capital allocation process. This is why people are starting to lose confidence. The counter thesis, summed up nicely by Bill Freeza is worth thinking about: “There isn't a person outside a mental hospital or an Ivy League faculty who believes the federal government can continue on its current fiscal trajectory, even with tax increases. Change is inevitable. Real change…”

In contrast to the deep thoughts of Mr. Summers, let me summarize a recent conversation with a former CEO of a high tech manufacturer of sleek, large ticket complex products that are fun & go real fast: ~ “How do they expect companies to allocate capital & invest for the long term? Or intermediate term? Do they think clarity on taxes for a year and a half is going to cut it?” That comment went on to a mutual discussion of the uncertainty induced by government in respect of just about every strategic & tactical consideration in virtually every private capital investment decision:

- Fiscal policy

- Monetary policy

- Energy policy

- Environmental policy

- Tax policy

- Rule of law, contract & property rights

- Immigration & labor policy

- Education

- the entire structure of the health care & pharma sectors

- the entire structure financial & insurance sectors

- State & municipal sectors

- Trade policy

Aside from the uncertainty, what is certain, what we do know looks bad. Invest now? Where do you put that factory? Why? For what return? For how long? Or invest elsewhere? California, South Carolina, Texas or China?Or just hang around the hoop to see what happens next year? The top line isn't going anywhere...

So we, like Roberto Durand, affirm our call, “No mas.” Hold the line for large scale spending reductions and regulatory clarity.

- the proposal will work, it presents a viable solution

- the present value of the benefits in whole outweigh the costs

- there are no better solutions and/or the proposal presents a least worst resolution

We expect our proposal to be dismissed by some as outright imbecility, induced perhaps by a pint of gin that Mencken somehow left unconsumed. But we conclude there is no viable mechanic other than the harsh discipline of the capital markets to fix the problem in the near to medium term. Further, unless it is fixed promptly, the adversity of compound interest & unfavorable demographics will make the future costs of solving the problem far greater or worse, push us past the point of no return. And there is a point of no return.

With few exceptions the political class, Congress, and the Obama administration have no inclination to even view the current and near term fiscal status of our country as a problematic: they in fact engineered a large measure of it. One suspects from their perspective it is a desired outcome from which a variety of preferred social justices self-directed emoluments can flow. Seemingly, the status quo presents no problem, it is a desired outcome or certainly a predictable outcome of certain policy goals that were pursued without regard to cost or fiscal prudence. Those costs now threaten the viability of our nation.

Refresh your knowledge of the magnitude of the problem

We invite readers to examine the structure of our current problem and understand its magnitude by looking at the pictures in our prior posting here: The USA as a business: say it with pictures

We are losing quickly the ability to grow out of our problem, and the probability of any viable timely political solution declines by the moment. The discipline of the capital markets will come: we need to harness it to bring about a viable solution.

Everyone has heard about the ‘debt’ crisis, but everyone needs to understand that the ‘debt’ crisis is the least part of our problem. Our unfunded liabilities are totally out of control and have reached a threatening magnitude.

To personalize the numbers, your household share of unfunded liabilities is estimated to be in the ballpark of $516,348.00 (as in the humble USA Today). Bear in mind the estimate is probably low, so the real nut is higher…for you. Further, consider that most of the households in the US simply can’t fund their share, so will your share get larger or smaller?

The cost per US household of unfunded promises made by federal, state and local governments:

|

Medicare Social Security Federal debt Military benefits State and local debt Federal civil- servant benefits State and local retiree benefits Other federal obligations Total |

$255,280 $144,251 $43,380 $25,863 $17,537 $14,374 $13,114 $2,548 $516,348 |

Check the investing & capital markets

Watson Wilkins & Brown removed some time ago, in the main, all US Treasury duration from its portfolios (yes, before Bill Gross’ call). We are not alone. Bill Gross of PIMCO dumped all Treasuries from the Total Return Bond Fund, the world’s largest bond fund, and many domestic fixed income managers have followed. Now we see dramatic short positions as the Financial Times reports:

at the beginning of this week, Reuters reported that Jim Rogers – co-founder of the Quantum Fund with George Soros …– planned to short-sell US Treasuries, as the end of quantitative easing removes support for government bond prices. Bill Gross – co-chief investment officer of Pimco – had already reached that conclusion, increasing his short position in US government debt in April. As a result, short positions in six to 11-year US bonds are approaching the May 2008 record level of $32bn, according to the New York Federal Reserve.

Look at the comparative spreads (as of approximately May 5, but close enough) of sovereign spreads in the credit default swap market:

|

Country |

5 year CDS% |

|

Norway |

16.5 |

|

Sweden |

24.3 |

|

Finland |

28.6 |

|

Denmark |

29.4 |

|

Germany |

40.2 |

|

Hong Kong |

43.9 |

|

USA |

49.3 |

|

Australia |

51.5 |

|

New Zealand |

62.7 |

|

Austria |

64.6 |

|

Chile |

67.7 |

|

China |

73.2 |

|

France |

76.3 |

|

Czech Republic |

77.4 |

Check the maturity structure of US debt and calculate what impact an increase in interest rates will do to coverage and service ratios. The Fed’s capital is ephemeral. Consider that debt is now X% of GDP, debt service is Y% of GDP, that taxes are Z% of GDP. So for grins, do a quick & dirty static analysis: you have to increase taxes by Y-Z% right out of the gate, just to stay even, not reduce taxes.

The May 23 Financial Times tells us that Bond Fund Flows Signal Shift. Ok, what does that mean? “Some emerging markets countries are now judged to be less risky than several western European countries.” Emerging markets debt “is no longer a niche…it’s losing its risk premium as the developed world has shot itself in the foot. Fundamentally, emerging markets are just less leveraged, and thus more able to repay their loans.”

A sober assessment of the political situation - a walk down Imbecility Lane:

The May 5th Companies & Markets section of the Financial Times carries the headline, Cheap gas threat to wind farms: “ ‘Ignacio Galan, chief executive of the Spanish energy group Iderdrola said the rise in US shale gas had transformed the country’s energy industry, driving down gas and electricity prices. ‘Shale gas makes the production of electricity from other sources not attractive…’”. Notwithstanding US federal tax credits and legal standards for renewable energy adopted by 29 states, ‘It’s hard to make an attractive return on investment’. Wait a minute? Didn’t we just pour boatloads of stimulus money down that rat hole? Hasn’t the EPA/DoE effectively shut down new energy exploration & drilling?

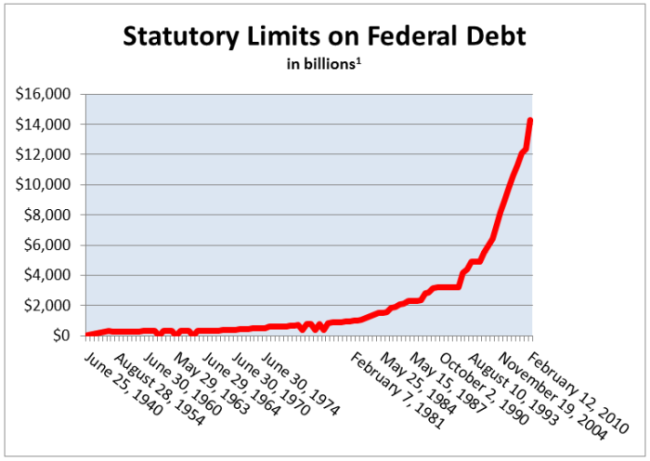

Statutory limits on federal debt: now, how does this work?

I just got off the phone with a very nice analyst from the GAO. I asked if there were a time series of data that compared the statutory limit on debt with the actual history of total federal debt. She was unaware of any such time series but guided me to a very helpful report from which I have made a very helpful picture:

By what construct are we to expect “debt limits” to work? We can see not only what the limits have been, but also how effective they are at limiting debt issuance or spending, which is to say not at all. And, of course, this being the government, you need also understand that the statutory limits on federal debt don’t really include all federal debt, but only the most favorite kinds (for example, TVA debt is omitted. Where else is Waldo?). Federal debt, of course, also does not include any off balance sheet unfunded liabilities (you know, all your social and medical benefits to be paid out of some non-existent, vapor filled ‘trust fund’ or ‘lock box’?).

But we wander: even though we have limits on federal debt, the limits don’t work. One hypothesizes they were never intended to work, but merely to provide a ministerial procession, another media event on the way to more debt.

We select the hard cap and the ensuing probability of default as we have concluded there is no viable political means of constraining spending. Yes, by the way, we have lost confidence in the quality of leadership & policy.

The discipline of the capital markets

“I regret to inform you that we have been unable to secure sufficient bids from our investors for your paper. We are attempting to find new investors for your program; however, we are not currently optimistic of success absent a significant and demonstrable improvement in your credit profile. We have offered the paper at the higher yields as you had previously authorized and regret that the pricing increase was insufficient to induce new investor capacity. We are currently not in a position to increase our internal inventory limits. Anecdotally, we are hearing of secondary market activity away from us at significantly higher levels.

We look forward to working with you to restore liquidity & discipline in the market and certainly will keep you current on any new developments. Likewise, please inform us immediately if you have any new information. Going forward, if you’re receptive, we’re happy to arrange & host meetings with a few key investors so you may receive the feedback directly… but in the meantime we anticipate, unfortunately, no change in the status of demand.”

I’ve had these discussions with sovereign states and corporate entities. They don’t much like it. Some try to get you fired, but it doesn’t change the bid or lack of one. Any crisis manager will tell you that organizational (or national in this case) denial is hugely problematic as it prohibits solutions. An addict will tell you, “It’s not a problem, I can stop whenever I want.” The corporate or sovereign treasury will tell you, “Investors don’t understand our credit [insert here the list of credit issues which are deemed by the issuer to not be problematic]... we’re much better than we appear.”

Hmmm… sounds kind of like setting a statutory limit on federal debt which has been and will be chronically reset or perhaps like the French finance minister commenting on the possibility of a Greek restructuring: “A restructuring, or rescheduling, which would constitute a default situation, what we would call a credit event, are off the table…” [said] Christine Lagarde, the French finance minister, “we are not debating that”.

That’s true. They’re not debating it, but, as others have pointed out, the rest of the market is. Ms. Lagarde will debate it when forced, when the bid stops. Investors understand that statutory debt limits will be chronically reset, that politician’s will kick the can down the road. The problem is that no one knows what, where, how or when the market will apply a real hard cap, or what the catalyst may be, the straw on the camel that triggers the chaotic, non-linear response of increasingly less stable equilibria.

Generally, the sequence is a technical default, then a substantive default, then some creditors throw the bankruptcy flag, and presto, there’s a change in governance & in behavior. Most of the time there is only change because there is no choice: such is the nature of and pricing in the market of governance.

The Druckenmiller Hypothesis: piece of paper #1, Monty!

Excerpted from the Wall Street Journal, What If the U.S. Treasury Defaults?, of May 14, 2011:

"I think technical default would be horrible," he says from the 24th floor of his midtown Manhattan office, "but I don't think it's going to be the end of the world. It's not going to be catastrophic. What's going to be catastrophic is if we don't solve the real problem," meaning Washington's spending addiction…the Treasury borrowing committee letter speaks about catastrophic financial crises, comparing it to Fannie and Freddie. That's not what we're talking about here," he [Druckenmiller] says.

"Here are your two options: piece of paper number one—let's just call it a 10-year Treasury. So I own this piece of paper. I get an income stream obviously over 10 years . . . and one of my interest payments is going to be delayed, I don't know, six days, eight days, 15 days, but I know I'm going to get it. There's not a doubt in my mind that it's not going to pay, but it's going to be delayed. But in exchange for that, let's suppose I know I'm going to get massive cuts in entitlements and the government is going to get their house in order so my payments seven, eight, nine, 10 years out are much more assured," he says.

Then there's "piece of paper number two," he says, under a scenario in which the debt limit is quickly raised to avoid any possible disruption in payments. "I don't have to wait six, eight, or 10 days for one of my many payments over 10 years. I get it on time. But we're going to continue to pile up trillions of dollars of debt and I may have a Greek situation on my hands in six or seven years. Now as an owner, which piece of paper do I want to own? To me it's a no-brainer. It's piece of paper number one."

Well, there’s another more important question besides which piece of paper do you want to own. How about as a citizen “in which scenario, in what kind of country, do you want your children to live?” Do we really think the present value of the short term costs of near term technical (or substantive) default will be greater than the present value of long term costs of letting the problems compound forward?

"the whole aim of practical politics is to keep the populace alarmed (and hence clamorous to be led to safety) by an endless series of hobgoblins, most of them imaginary." H.L. Mencken (In Defense of Women)

This is the existential dilemma ... 'we can't go forward, we can't go back, and we can't stay here'... put forth by Geithner and Summers. I don't buy it. We can fix the problem. Stop putting my kids and all of us in debt. Fix the long term structural problem now.

If we have to push it to default to fix it, ok. We're dealing with large scale costs either way. My bet is that it's cheaper to fix it now. My take-away is that every investor and citizen should re-read At Dawn We Slept. This is a story about a fundamental failure of the republican democracy of the United States of America, of political leadership left untended and unsupervised by the voters for too long.

We concede this is a bit out on the edge for us, perhaps skating too close to the edge of the ice of politics. However, the degree of governmental control and interference with market function will have a material impact on economic and investment outcomes for the next several generations. It's hard to opine on whether to plant wheat or soybeans when the fields are on fire. Perhaps we put out the fire?

This ends my agitation... for today.

________________________________

1 May have dropped one or two data points which the dullard analyst could not cipher.

hb

hb

If interest rates normalize over that period [the end of the decade] the added interest costs in 2021 alone will be $800 billion—more than 20 times the mere $37 billion in budget cuts that tore up Congress in March. It would take virtually all of the cuts in the Ryan budget just to cover that added interest, much less to start bringing down the national debt. Unfortunately, the Fed is now in a fiscal box. A normalization of interest rates would break the Treasury." - Lawrence B. Lindsay in WSJ June 15, 2011

"After one gerneration, a one percentage point difference in the [economic] growth rate becomes a 25% difference in per capita income." Allan H Meltzer, A Welfare State or a Start-Up Nation?, WSJ of June 15, 2011

" [default] could cause sever disruptions in financial markets and the payments system, induce ratings downgrades, create fundamental doubts about the creditworthiness of the United States, and damage the special role of the dollar and Treasury securities in global markets in the longer term" - Ben Bernanke in the Financial Times of June 15, 2011

Mr. Bernanke has evidently failed to notice that he is radically behind the trade on each item in his check list: everything is pretty much cooked to medium-well right now.

- Ratings downgrades - already on notice. The notion of the US Treasury as "risk free" is decimated. Look at the CDS swap spreads.

- Fundamental doubts about the creditworthiness of the US - see above.

- Damage the role of the US $ - has the current price of the US$ escaped the attention of the Fed? Or the price of gold qua an alternative currency?

Reader Comments (1)

I agree: Paper #1 is by far the better choice. I agree that the discipline of the private markets is far more reliable than governments. I also think that your quotation from Mencken's "Defense of Women" is apt.

I have been encouraged by the leadership in the House, and I should like to see considered a constitutional limit (with escape clauses for genuine emergencies) on the proportion of debt to GDP. Clearly (at least for me) eliminating all debt would prohibit mutually beneficial exchanges between overlapping generations. Thus, we do want some debt. And limiting debt to a proportion of GDP makes sense to me.