Caedite eos! Novit enim Dominus qui sunt eius

We probably should talk about investments, although what I want to do is rant about our domestic policies which are destroying so much of our economy, so much of our national value. We'll get to both, and pictures are a good place to start.

This year's markets were uninspiring at best, frightening at worst. US equites struggled to hold near even while foreign markets, both developed and emerging, suffered. As always we select broad indices for illustrative purposes and note these are graphs of prices, not total returns.

Segmenting the domestic markets into large and small cap sectors is not particularly instructive:

But changing the time frame makes a considerable difference. Investors who were out of the market for the last two years missed a significant restoration of value:

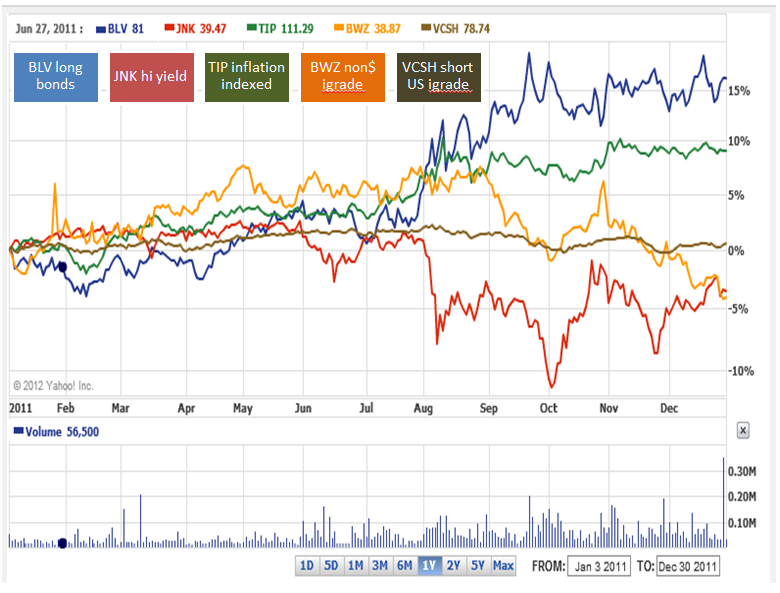

Fixed income markets were almost as volatile which in itself conveys an important message:

Our macro view going forward

Regarding credit/counter-party performance risk we remain very suspicious of whatever is highly regulated, complex, and opaque... Europe comes to mind....and for that matter CDS risk, the regulation of the repo market, Congress itself & the entire financial sector. If you read Currency Wars, you will wonder along with me which snowflake causes the avalanche?

We face higher probabilities of polar outcomes, at one end the world as we know it continues a long term, uphill structural struggle with slight improvement. At the other end of the spectrum we actually find out which snowflake caused the avalanche, and that is a dark scenario.

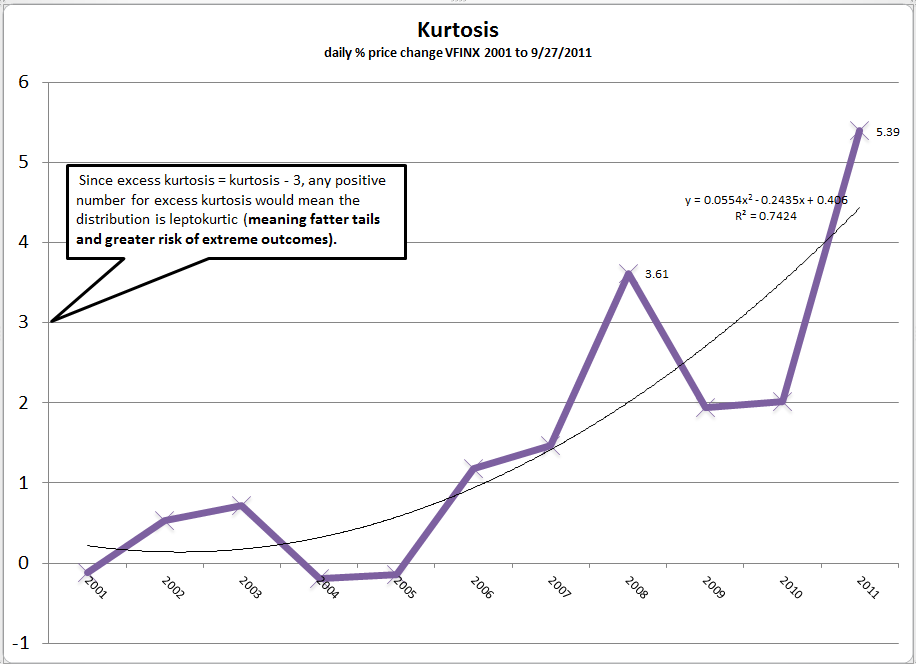

Our thinking as to risk is framed by a previous analysis that details the annual kurtosis in the daily returns of a proxy for the US market, Vanguard's S&P 500 Index Fund.

If the world continues without a Great Unpleasantness, we’re comfortable with our outlook as stated in August, although we might modify it as marked:

Look for nominal growth of 0%<GDP<2 2-3%, if not a few quarters of negative numbers. We expect employment will go sideways to nominally up, but would not be surprised to see that, too, go negative from time to time. We anticipate corporate capital budgets will be trimmed, limited to only near term high certainty payoffs or strategically important or competitively disruptive initiatives. Emerging markets may continue to attract new capital investments on the margin, but that goes away in a heartbeat if corporations see uncertainty in global demand: “Who shall buy these widgets?”

Our sense is most corporations are building in 1-3% nominal growth to their baseline plans with ‘stretch’ incentives leveraged to the upside. There is anecdotal evidence of some broader optimism in the corporate boardrooms. M2 is growing about 10% year over year, but M2 velocity is dropping like a stone which is not good, if not very bad.

On equities:

At the risk of political catcalls my plain view is that the US equity markets (take VTI as a proxy) will be highly & negatively correlated in a non-linear way to futures contract pricing Barack Obama’s re-election.

The plain fact is that there is considerable economic upside to be priced in the

- rationalization of the tax code,

- reduction of regulatory burden, and

- the loosing of the choke hold on the development of secure, abundant domestic energy.

Without a change of administration none of this value will be realized, and the value destruction will continue. Hence, strong negative correlation.

Consider the economic impact of stable or declining long term energy costs and the re-direction of petro$ flows to domestic investment, away from nations who seek to harm us. Just as natural gas might be of sufficient magnitude to revitalize the mordant, overspent economies of Pennsylvania or New York, abundant domestic production might very well hold the same possibility for our nation in a time of acute need.

We’re not in the business of forecasting (at least correctly) but given the wall of worry currently built into this market we could easily envision a scenario of the Dow pushing 15,000-17,000 or significantly higher in a best case outcome. A PE of ~12x on the S&P is not the unattractive part. One might hypothesize that technology has significantly increased the ability of corporations, even smaller ones around the world, to measure operations, manage risks & redeploy capital more quickly & effectively than in the past. It is a skill we might need.

Perfect outcomes are rare, and the real issue is the risk thresholds through which we pass in the hope of getting there, and you may read that as kurtosis or systemic risk or call it whatever jargon you like. On the downside, we must recognize that the risks we face are very real, and if the value destroying policies are left intact we see the possibility of as much as a 10% retrenchment in US equities, continued uncertainty, 0% to nominal job growth, rising unemployment, and minimal domestic investment…in short the grinding process of lowering the American standard of living. We will speak to the downside of systemic risk and the Fed’s role later. It is real.

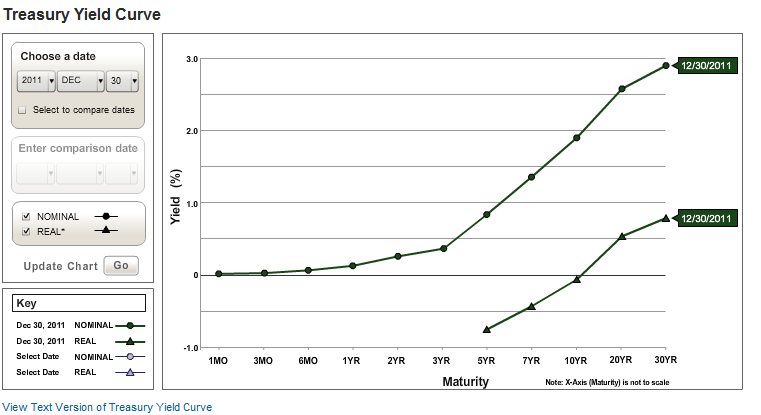

source: US Treasury website

The negative interest rates (triangles above) have the consequence of inflating asset values across asset classes (cost of capital down, values up). It is harder to discern where home base is, harder for those charged allocating capital to know current values and future costs. While we argue that a market PE of 12 or so is not unattractive, but it’s getting harder to tell. Call it the fog of market manipulation. That’s the diffusion of accurate price/value information that impairs capital formation and investment. Consider the inherent logic of negative rates as a risk utility, a statement of risk preference: give us a dollar today and we will give you $.97 back next year. That's the deal investors are taking in size.

Everyone knows US corporations have lots of cash and for very good reasons:

- Liquidity is good if you don’t believe that your Euro banks, and perhaps others, can or will honor their funding obligations to you or otherwise present significant counter-party risks. Who is providing whom liquidity?

- You don’t want to invest in long term assets when you have no clue as to the tax or regulatory environment attaching to those investments. It’s a hard way to fly.

- Lastly, you can’t repatriate cash to invest domestically without paying a whopping tax, and we like cash, yes?

The Euro thing is pernicious. If forced, we might consider a SWAG mark down of 20-25% of all Euroland enterprise value not unreasonable, but timing is everything. Consider that iShares MSCI EAFE Index Fund (ETF) EFA is down about 40% from November, 2007. Pretend you’re a dog pretending not to see another dog, which accurately characterizes our position.

Domestic dysfunction of leadership & feeding at the trough

Let us count the ways, Congress. We shall start by noting in the Wall Street Journal the magnitude of Congress’ desire, intent and capacity to monetize its ability to dispense economic privilege. It mostly takes the form of from Thee (the taxpayer) to Me (the politician): In Capital, Investors Pay for Trading Tips.

It represents the degradation of rule of law. It is not new but regrettably well known to market participants and politicians. Congress exempts itself from so many laws it imposes on citizens. No worries Mr. Congressman, you and your staff are free to trade with no pesky black-out periods or SEC Well’s notices.

Unfathomable & destructive tax code

The CCH Standard Tax Reporter now fills 72,536 pages to fully document the US tax code. A simple example: ask your tax advisor to clarify the “substantially similar” test in respect of the Wash Sale rule used to offset long term capital gains & losses. You will have a conversation that goes something like this:

Q: Is this “substantially identical”

A: Don’t think so, but dunno.

Q: How does the IRS define it?

A: They don’t.

Q: Will this be OK?

A: Think so, but dunno. We can research it further.

Q: No thanks. Anything else?

A: Here’s my bill. Have a nice day.

The disarray is not limited: pick a card, any card.

No budget

We are now almost three years without one. The Senate has not passed a budget in some 900 days. Or consider the manner in which the recent 1,000-page omnibus spending bill was posted online Thursday morning, without an official Congressional Budget Office Score showing what it would cost, and rushed to a vote on in the House on Friday afternoon.

The Fed

*DUDLEY: FED HAS LEGAL AUTHORITY TO BUY FOREIGN SOVEREIGN DEBT

*DUDLEY: BUT BAR TO BUYING EUROPE SOVEREIGN DEBT VERY HIGH AND

*DUDLEY REITERATES FED NOT `CONTEMPLATING' MORE AID TO EUROPE

No audit, no control, no transparency of swap lines, gold loans, or other off balance sheet contingent exposures. The Fed’s view: we do as we deem best. No enumerated authority needed, requested or desired. Need we say more? Well, we did in September 2011 in The ECB Thing (excerpted below). Our speculation was well in advance of the WSJ’s Dec. 28, 2011, article The Federal Reserve's Covert Bailout of Europe.

The reason you can’t conceive of how the ECBThing [or euroanything] works or makes sense is that it doesn’t. It cannot work unless Germany, France and all the others including the US all play for size (recall the word “overwhelming” by Timmy Geithner, you know the fellow who said there was "no risk" of a downgrade for the US?). You think, "no way US taxpayers would support committing of huge amounts of scarce US (read that taxpayer) capital to such a venture!"

But consider that the Fed and Treasury may not be concerned with that quaint notion. It is likely we're already in for size, such and duration to be expanded and defined later. Since it's election time how about a Congressional hearing or two? A little transparency on swap or currency line usage or risk limits? An audit?

The Fed defines Eurothing counter-party risk as zero, and this notion appears to be a disinformation program directed towards the citizens of this country. The risk is not zero, the markets know it (as by the liquidity and solvency crisis in the first place), and the Fed knows it. Consider the wisdom of the same mentality: "on the basis of historical experience, the risk to the government from a potential default on GSE debt is effectively zero" [Implications of the new Fannie Mae and Freddie Mac Risk-Based Capital Standard by Robert & Peter Orszag and Joseph Stiglitz, 2002]. It is creating a non-trivial credibility problem and tenuous risk profile in the markets.

Lastly, the Fed again: an Alfred E. Neuman moment receives no public attention

“The main purpose of this paper is to provide an overview of data requirements necessary

to monitor repo and sec lending markets, and so inform policymakers and researchers about

firm-level and systemic risk….we find that existing data sources are incomplete”

source: http://www.newyorkfed.org/research/staff_reports/sr529.pdf

You read it here first, folks. Note the date: December 2011. This publication is an implicit and public admission that what you and I (as semi functional and soon not to be sober proxies for the Prudent Man) would agree as fundamentally basic & necessary, but perhaps not sufficient, information for any kind of risk assessment is simply not available to the Fed.

One might then reasonably inquire as to how and on what rational basis ... other than that to be found in a room, dimly lit by burning candles, with chalk pentangles and splatters of chicken blood on the floor ... how do they evaluate risk of this market which funds, essentially, the entire financial system of the known world?

One of the conclusions emerging from the paper is the need to better understand the institutional arrangements in these markets. To that end, we find that existing data sources are incomplete...

Specifically, we argue that six shared characteristics of repo and sec lending trades need to be collected at the firm level:

1. principal amount,

2. interest rate,

3. collateral type,

4. haircut,

5. tenor, and

6. counterparty.

In addition to the above, we believe there would be value in collecting data at the firm level on the instruments in which securities lending cash collateral is invested. These data would create a complete picture of the repo and sec lending trades in the market, and so allow for a deeper understanding of the institutional arrangements in these markets, and for accurate measurement of firm-level risk. Further, these data would allow for measures of the interconnectedness of the repo and sec[urities] lending markets, which allow for better gauges of the systemic risk in these markets....

OMG. Hey, guys, what have we been doing for the last decade or so? First, Fannie & Freddie, then the bail outs (AIG’s CDS book and all the counter-parties). Then MF Global (Hey, Gary, what’s this co-mingling thing again?) with the further revelation of unconstrained daisy chains of re-hypothecation (oh, btw, its okey-dokey from a broker-dealer compliance perspective, we understand). Mis, mal, or non-feasance, and now the informational void of necessary risk information for the entire repo market, which, we would add parenthetically, is the only surviving source of liquidity for our broker-dealers, most of the banks, and all Europe.

This evidence supports several conclusions:

- Regulators do not have a clue, but they tell the public they do.

- They don’t even have the data to get a clue.

- The myth promulgated by the government and regulators that "regulation = safety" is simply false and misleading. And destructive.

Solutions

We seemingly face a meta crisis of confidence, impacting nearly all forms of leadership & rule of law. Beneath the surface, every form of agency risk is suspect. We have passed the point of diminishing returns of complexity & value in things political, legal, and regulatory. The solutions start with simple but big things.

Understand & remedy the smarty pants problem, also known as Hayek's information aggregation problem, or failing that, call it simple arrogance. Government and the people of government are neither smarter nor more ‘moral’ than the markets. Government tends to be equally corrupt, if not more so, and the bureaucrats not only distain but lack the ability to aggregate information and hence are always behind the trade.

The biases of the smarty pants problem is foundational to the Fed which by policy creates a host of unintended consequences. Consider the Fed's strategy (and other regulatory initiatives) of trying to manage excessively large and stupid concentrations of risk (i.e. "too-big-to-fail") by further aggregating and centralizing even bigger concentrations of stupid, unknown & unmanageable risk. This transforms “too big to fail” into “too big to save”. And chaos may well determine the precise timing of that transition to poverty. Hope is not a strategy.

Move to dis-aggregate the risk. The current arrangement has us, meaning we the people, in the cross hairs of a .50 caliber or MOAB. Perhaps we arrange institutions so they, not we the people, get shot by smaller bullets? In order to do this you will need to dis-aggregate risk, which is doable by addressing the moral hazard brought to us by political corruption and cultural decay. However, the good news is that Moore's Law is still on our side.

A thought experiment, in process, but good enough to go: let's convert the Post Office from mail delivery to local branches of the US Treasury. They have lots of nice locations & nice people. The new function would be to maintain demand deposit accounts for individuals (and only individuals) seeking full faith & credit of the US Treasury (what previously was known as the origin of the risk free rate). Tell the public, no more risk free lunch. Announce that no other institution has any protection, real or implied, whatsoever. Make institutions compete for capital on the basis of the risk they create & manage. Heave a few on the bonfire to make some examples. Folks will catch on quickly.

Eliminate requirements for and priviledges of Nationally Recognized Statistical Rating Organizations and leave them to their shareholders. Leave fiduciaries to their diligence. Timing & such to be worked out, but you get the drift. Banks could do whatever, say, CDS's without limit, and depositors & investors could do whatever diligence they deem appropriate. Terminate every regulator associated with the current banking system and delete the majority of that entire body of law. Three hundred and sixty days or so to no more moral hazard?

End the disinformation program. Our leaders need to start telling the truth. Acknowledge and address the fundamental issue of ‘no free lunch’. There is no risk or cost free solution for anyone or any institution. European sovereign debt has credit, currency, liquidity, and performance risk associated with it. Long duration Treasury bonds have risk. Acknowledge that n x n matrices of gross and net CDS exposures devolve to gross as counterparty default risk rises. Acknowledge that Social Security is a Ponzi scheme by any common definition of the term. The clarity of language allows the fix.

Citizens must require ethical leadership: Consider well the inspiration & intent of leaders: "Conscience is the virtue of observers and not of agents of action." - Sol Alinsky. Don’t vote for unprincipled leaders.

RIP 2011 and thus ends my rant. Keep the faith. hb

hb

hb

Bill Gross in Toward the Paranormal of Jan 2012 (also released yesterday, we think) echoes the same fundamental themes and in fact some of the same language:

- the increasing probability of polar outcomes and wider tail risks

- the fallacy of risk free sovereigns

- low to zero nominal rates / negative real rates

He has been infected with and characterizes the meta crisis of confidence we describe. We do not celebrate a confirmation of our diagnosis.

hb

In a letter to the editors appearing in today's WSJ, William Dudley responds to The Federal Reserve's Covert Bailout of Europe. Unwittingly, he defines the problem perfectly:

"The intention is to ensure that financial institutions headquartered outside of the U.S. that are deemed credit-worthy by their central banks have the dollars they need to fund their U.S. dollar assets and activities."

"...These measures are meant to create a credible backstop to, but not supplant, private markets..."

All along we thought CDSs, direct pay letters of credit, high quality collateral, or back-up lines of credit were intended to be credible backstops or protections. But that is so yesterday, isn't it?

We have highlighted the problematic parts. The prompt response by the Fed suggests some sensitivity as to credibility. We leave it to our readers to decide why.

hb

Bank regulators: a little behind the repo trade don't you think? See our reference to the Fed study above.

Heat's on Triparty Repos 5/4/2012

Reader Comments (3)

Tu es Petrus et super hanc petram aedificabo meiam ecclesiam. Et tibi dabo claves regni caelorum.

Great hearing from you. Come visit me in England one day.