A little more perspective

Our last posting, A Bit of Perspective regrettably promised further thoughts on recent market events, so here we go. First time readers may want to take a quick look at the graph in the original posting. It is our starting point.

We are not unduly troubled by the recent volatility in the market. You have to place it in a longer term context of a huge bull run in equities & the perils of the Fed artificially fixing prices for a long time and then changing its mind. So, we wash out some levered players, and some folks start to get a clue as to the perils of duration. We don’t mean to be dismissive because we do watch this closely, but it’s not the short term noise that gets our attention, it’s the underlying tectonics.

The key issues are quite large, and no one in government is asking, or we might hypothesize has the capacity or inclination to understand, let alone fix.

We start a simple question, “What caused the damage to the fundamental fabric of the real economy?”

Let’s consider the magnitude & differences of

- the decline of the markets starting in January 2000

- the catastrophic collapse of the markets in July 2007

The blue is Vanguard’s S&P 500 Index fund which we take for our purposes here as a proxy for the entire US equity market and as a further proxy or footprint of our real economy. These are very big and catastrophic downdrafts.

https://www.google.com/finance?q=vfinx&ei=FoTIUYDJO4Xe0gHVfA

Note the absence of capital markets failures as an outcome in the Jan. 2000 decline. For warm ups, recall the meeting of money center banks in NYC called by the Fed in September of 1998 to sort out the troubles of Long Term Capital Management. The solution was semi-voluntary infusion of capital effected by a fire sale acquisition orchestrated by the Fed (note all the surviving banks became Too Big To Fail later on). The capital markets were stressed to be sure, akin to a near miss of a crash or a brief power outage, but a sufficient amount of capital & liquidity was raised among the related players to cover the risks. A bit later came the crash of the tech sector and a lot of investors lost money, but nothing else much happened. A bubble burst and the equity & liability holders who took bad risks took a bath. Not pleasant, but not contagious.

The demise of Long Term Capital Management had explicitly revealed the seeds of a very different problem, excessively leveraged & widely distributed counterparty risk. No one knew who, where, how much or what the matrix of counterparty exposures ultimately looked like… including the regulators. The nature of the trades & structure of the implicit mis-match of asset & liabilities were leveraged >50x. As the assets declined in value the leverage increased, at deathbed to about 250x. The global markets were hit by the tsunami, but the flood walls held.

All the CEOs of the money center banks involved in the Sept. 1998 meeting had massive institutional risk to and, interestingly, most if not all, had some degree of personal investments in LTCM. The nature & structure of informational voids, the magnitude & distribution of consequent exposures were made clear to all at the table.

In the largest failure of prudent regulation and financial risk management in modern finance no significant or effective regulatory effective response eventuated. On the corporate risk management side, no solutions were forthcoming to the very real, large & freshly demonstrated problem of managing a dynamic global matrix of derivative and cash counterparty exposures while a significant number of the counterparties start to fail. Everybody in the room including the regulators knew that an N x N net matrix of exposures devolves to a gross matrix when the participants start to fail. And the gross numbers were staggeringly large… unthinkably so, but there they were.

Let me repeat. No significant structural changes were made to the essence of the problem: the mis-match of reward fueled by >50x leverage provided by the banks and other market participants. It was clear that the ability of the banks to fund such activity was ultimately enabled by a faulty risk management framework and flawed regulatory framework that had at it's base moral hazard (taxpayers via the US government). The deposit base and the regulatory framework enabled the ability to fund the massive risk, now made clear.

The catastrophic failure of the global markets is the key distinction from what happened in 2000 & 2007. Left to grow & compound the risks evident since 1998 were amplified by the US government policies, particularly the virtual (90%) monopoly of Fannie Mae, a Government Sponsored Enterprise, in the mortgage markets, and the exponential growth of the derivatives market. Of course, in decade preceding the collapse of 2007, the GSEs spent at least $171 million on lobbying, which combined would make Fannie and Freddie the third-biggest lobby (WSJ, July 17, 2008). It is unsurprising that Fannie & Freddie assumed the role of the rent seeker, Congress monetized their requests and accommodated with ill-conceived policy to amp the volume and disregard the risk, particularly for low quality loans (you may recall liar’s loans or Alt B loans as that special form of social justice). Aiding and abetting we might otherwise call it. The lobbyists’ money came in; the politicians cleared the decks; Wall Street leveraged the party and distributed the product globally. The systemic risk accumulated on balance sheets (the matrix of unthinkably big numbers) and long term assets were funded with short term money (leverage). Then there was a little glitch, ‘really nothing, got it covered’… then ‘hey, this is serious!’ and then short funding collapsed in a systemic failure of the commercial paper markets (the source of liquidity) which threatened the entire global capital markets.

The Fed ended up buying it all, and that’s essentially where we are today. We recommend Reckless Endangerment: How Outsized Ambition, Greed, and Corruption Led to Economic Armageddon by Gretchen Morgenson for those interested.

The essence of the problem has not yet been addressed.

We have yet to realize those losses in full, and one suspects, at least by a quick look at bank & sovereign balance sheets, we have only made a partial down payment: more to go. Certainly, the Fed has tried its best paper over the hole in the wall, to cover & amortize the loss by printing money, but we have the weakest economic recovery in domestic economic history (thanks, Harry & Barry).

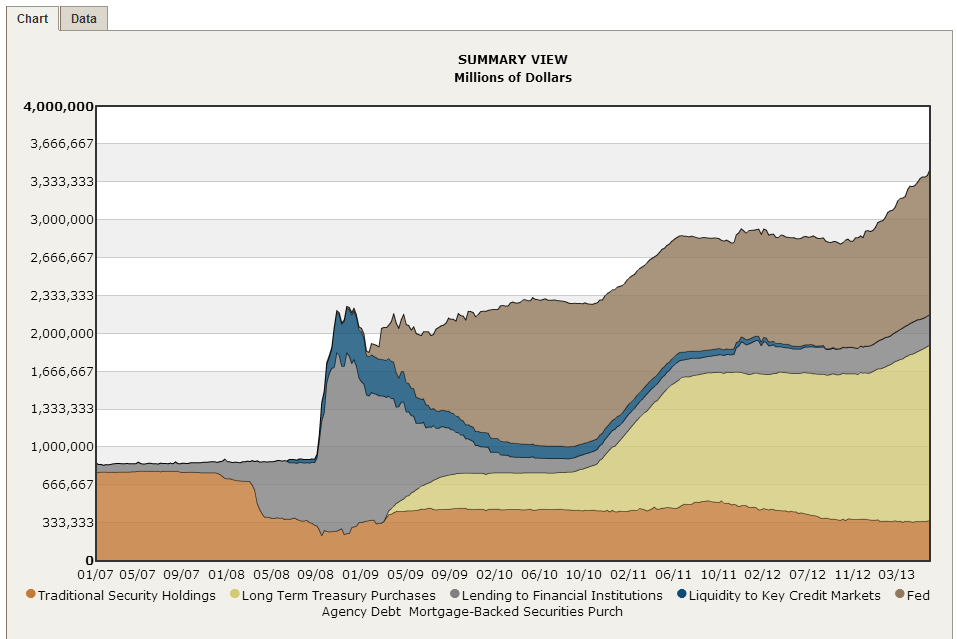

Notwithstanding a clear understanding of the root causes of moral hazard, nothing has been done. We are watching the full movie again, this time with the Fed holding all our eggs in its basket without limitation or audit. The source & structure of the risk has essentially not changed. It has merely been transported to the Fed by the Too Big To Fail institutions and the global central banks. Look, you can see it:

Courtesy of the Cleveland Fed from 1/7/2007 to 6/19/2013:

http://clevelandfed.org/research/data/credit_easing/index.cfm

The graph depicts balance sheet items only, off balance sheet risk items (I believe swaps and memoranda accounts of contingent or implicit guarantees of TBTF and whatsoever markets, commercial paper, notional swaps and repo come to mind are excluded. Perhaps a reader would advise or someone could call them and let me know?). In one sense it doesn’t matter. The numbers only get bigger.

The real economy is actually quite simple. Wealth is generated by making more useful stuff better, faster & cheaper, making it available to more people… efficiency, the process of allocating capital, human & financial, and letting the markets, which are aggregates of peoples across the entire world, do their thing on a voluntary basis free of fraud, violence & coercion.

Printing money does not facilitate this process, it distorts pricing. Screwing with the rule of law damages it. Corruption damages it. Friction costs (taxes and political corruption) damage it. Over time we hypothesize that opportunity cost can become real cost. Voila! Lower standards of living and a decreased opportunity set for the country.

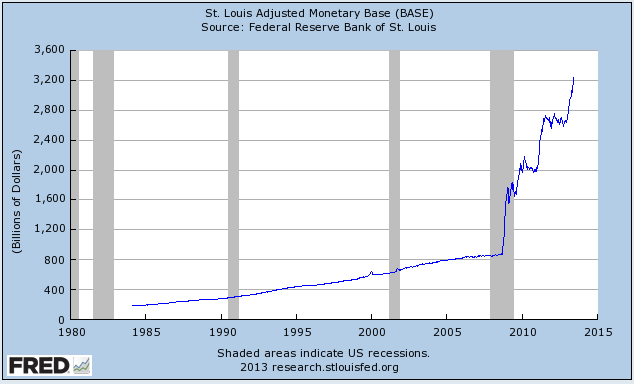

http://research.stlouisfed.org/fred2/series/BASE/

Governments, particularly stupid or corrupt ones, interfere with or thwart the process of making stuff better faster & cheaper. They aren’t good at letting the process move forward, but they do excel at moving backwards, destroying wealth by transferring it to unproductive outcomes (c.f. Euroland’s destruction of productive capital comes to mind… or the Soviet block) to manipulate political power.

Consider the major destructive economic issues of recent time:

- Systemic risk

- National debt, funded & unfunded liabilities

- Dysfunctional tax code

- Destructive regulatory framework

|

Issue |

Examples |

Progress/solution? |

|

Moral hazard (private reward underwritten by socialized risk) |

Too Big To Fail banking system Federal Reserve Bank US mortgage market US money markets ObamaCare MediCare 2 of the Big 3 auto companies. GE & et al

|

None. Getting worse: concentration of banking, shadow banking, and investment sectors. Estimated $1.2 quadrillion notional global exposure of world derivatives. Estimated $24.6 gross notional OTC derivatives 6/2010 Declining credit quality of US banks Manipulated monopoly of Treasury market & interest rates. Management of bank capital levels by mysticism & fiat.

|

|

Exploding debt & unfunded liabilities of government |

MediCare - $100 trillion unfunded liability Social Security - $18 trillion unfunded liability ObamaCare $17 trillion unfunded liability Detroit California Illinois Stockton, CA Harrisburg, PA

|

Increasing by the minute & surpassing the real economy’s ability to fund it. Unprecedented Fed experiment wagering “all in” amounts of our national wealth with no oversight.

|

|

Complexity & corruption of US & state tax codes |

~73,000 pages; of debilitating, onerous & costly compliance, constant changing Small % of citizens have skin in the tax game nationally

|

None, getting worse. Mis-allocation of productive capital Material costs of compliance & avoidance Corruption via monetization of legislative process Oppression of entrepreneurs Unproductive cost burden on businesses & citizens Loss of confidence in integrity government

|

|

Complexity, cost & dysfunction of federal, state & local regulation |

ObamaCare Dodd-Frank EPA DOL DOE et al $1.7 trillion annual cost of compliance

|

None, getting worse. Huge uncertainty Mis-allocation of productive capital Material costs of compliance & avoidance. Corruption via monetization of legislative process. Oppression of entrepreneurs. Loss of confidence in integrity of government Grossly negligent & reckless legislative process

|

All are plagued by uncertainty which freezes the status quo leaving inherently destructive processes that aggravate or allow the legacy problems to compound without limit. It is a failure of government. Or rather a government of failure. Congress & the Administration impair investment, liquidity & employment and increase systemic risk… essentially guarantying continued low growth while the problems worsen.

This is not genius at work.

The macro picture

The macro picture is screwed up and moving forward in an uncertain & debilitating way. If you ask most businesses and certainly any trading desk, they will tell you (or maybe not given the consequences of being identified as a critic of the régime, pay back being a bitch) that the biggest variable in their business is some form of government. The primary focus is no longer making widgets, buckets of bolts, soap, chips, new genetic therapies, new generations of robust crops for vegetable sourced protein, or very cool new small particles. Job #1 is to manage near term mortal or costly threats to your current business imposed by the government. Job #2 is to buy’em off or turn the hungry Leviathan towards your competitor. Or get your snout in the trough and have at rent seeking. Job #3 is to improve operations, invest or develop new products.

The economy, however, works best when you reverse that order. If you want the economy to work, you have to do things a bit differently. Effective leaders know that success in crisis requires the team to believe it can succeed in the mission. Acts in bad faith or breaches of ethics or law preclude that. So does stupidity. People no longer trust leadership, and there is a competent and growing body of evidence to suggest this harsh judgment is correct. People no longer believe the leadership of government, ours to be specific, is ethical or competent. They in fact may be right. As it stands now the US taxpayer is a bullet magnet for systemic risk, and it is lowering our standard of living.

Even the Fed knows it has reached the end of its rope.

“The market, in turn, isn't too keen on the thought of infighting at the Fed at such a delicate policy juncture as it suggests the Fed might not have the firm grip it professes to have on managing monetary policy.” - Yahoo Market Update June 24, 2013, 12.46 pm EST

The elephant in the room is essentially unchanged from 2000. Major pockets of insolvency have been created by capital destruction yet governments have attempted to hide the losses and defer the bad news of realization... faux policy at work. But both the losses and the sources of the risk remains.

Consider the real capitalization (on & off balance sheet items, risk adjusted) of the

- United States

- Federal Reserve Bank

- Too Big To Fail institutions (infinite do-loop of systemic risk)

- European, Asian & Emerging sovereigns & banks

One wonders: “Is there an intent of clarity of analysis or accuracy of disclosure?”

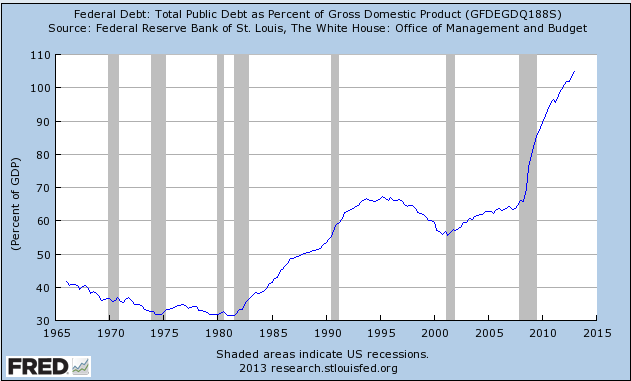

http://research.stlouisfed.org/fred2/series/GFDEGDQ188S?cid=5

Bit by bit, perhaps, but the main problems remain unchanged, and the political obstacles to resolution continue to grow.

Implications for markets: diversification & asset allocation remain key

In broad context of markets, our view remains unchanged with the exception that maybe even the Fed seems to have recognized, or at least superficially acknowledged the possibility, of limits to its strategy … at least this week. However, the Fed today is not the Fed of tomorrow, and Janet Yellen is waiting in the wings. View her resume. You will see a pure academic & apparatchik with no experience whatsoever in the global or domestic capital markets. One might infer an arrogance of faith based belief in centralized economic management that rivals, if not exceeds, that of Bernanke.

So, we anticipate

- a continuing slow grind of domestic “recovery”

- a continuing & increasingly delicate balance between inflation & deflation

- increasing peaks of volatility generated by governmental whimsy & occasional solvency crises

Our general posture can be described as a “least-worse” variant. We are not inclined to monkey with our broad allocations of fixed income and equity based on near term market fluctuations or headline risk, although we encourage all investors to fully understand their profile in that regard. We are inclined to examine closely the fixed income structure of our portfolios.

Implications for fixed income

We had an interesting conversation with a prospective client the other day:

Q: “If you knew interest rates were headed up, what would you do?”

A: “I would go all-in shorting 30 year zeros. But the question is academic. I don’t know that rates are going up and neither do you. We think rates are going up, but we don’t know for certain, and we do not know, nor can we know with adequate certainty, the direction, timing or magnitude of any such moves. It’s not a cost or risk free trade, and you have get all three mostly right to make it work. The practical outcome, depending on your confidence and ability to wear the risk, is to restack the fixed income to raise cash and shorten what duration you have. We are dis-inclined to bet the ranch on any particular speculative view.”

Direction, timing, and magnitude: the limits of knowledge. It is called risk.

Our guess is that the likely outcome is a period of rising rates. The Fed has manipulated interest rates and capital markets since 2000 and delivered the weakest recovery in modern history. The balance sheet of the United States is now over levered (including funded debt & unfunded liabilities) and unsustainably so. We have reached capacity. Detroit & Greece have amply demonstrated the fallacy of public finance: "[the] basic tenet of the $3.7 trillion municipal market: that states and cities will raise taxes as high as needed to avoid default". The analogy to the Fed is obvious, even to them. Shall we set aside for now the question of who would make such an idiotic assumption in the first place?

It is clear we have likely have reached a point of inflection on rates absent further intervention, and we see the Fed is getting a little chippy about the behavior of some market participants : Fed fights back against ‘feral hogs’.

So look for some volatility if, or rather when, a shoving match breaks out. You could see an object lesson in don’t fight the Fed, but we note the win/loss record of central banks vs. rational markets is not impressive. The chart below depicts the last six month prices of Vanguard’s Intermediate Bond Fund (red) and Long Term (blue) Government Bond Fund in ETF form. Holders of duration have been given a preview of the can of Whup Ass headed their way.

https://www.google.com/finance?q=vglt&ei=vZrIUYidLYXe0gHVfA

Our bias against duration will continue, and the risk of that bias is further Fed intervention. For now we’re comfortable with short duration investment grade product. The spreads have declined, but there is still some value and stability in the sector.

We urge caution on municipal bonds given what we perceive as systemic failures of disclosure (we would call it fraudulent), orchestrated by politicians. Unless you have direct access to the primary sources of actuarial analysis of pension liability and other off balance sheet liabilities you have to rely on the rating agencies. Look at Illinois; California; Stockton, CA; Michigan; Detroit, MI; and so on. Nuff said. There is, of course, a cost to restricting a whole class of assets but we’re prepared to accept it. No clear information, no money.

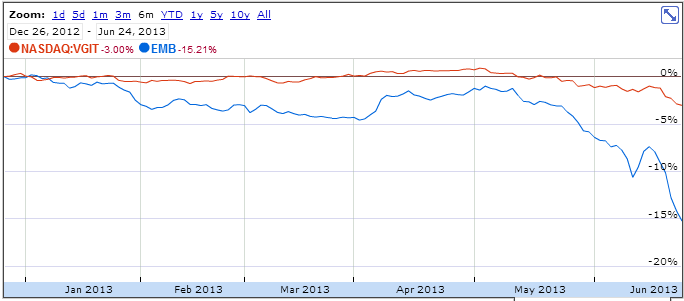

Emerging markets bonds have taken an impressive beating lately. We’re inclined to hold on the long term thesis that EM debt will become a viable substitution for developed markets as investment grade capital migrates out of Europe. We like liquidity premia, less fond of duration, so we’ll look short. Below, a six month relative view of prices of Vanguard’s Intermediate Government Bond Fund (VGIT) in red and iShares JPMorgan USD Emergent Markets Bond Fund (EMB) in blue. Not pretty.

https://www.google.com/finance?q=emb&ei=2JrIUaGZAump0AHYvAE

High yield credit quality will likely be stable in a sideways economy and may benefit from any more positive economic scenario. Like EM bonds, however, the duration will suffer under a rising rate scenario, so we may take a look at shorter duration or floating product. We have some concern about liquidity issues, so be prepared to hold what you buy or pay up to get out. It is a minor asset class for us.

Inflation indexed product

Again, we will likely be looking to shift to shorter duration indexed product. The mathematics of inflation indexed product is complex but, in a nod to angels dancing on the heads of pins, our sense is that shorter duration product will track near term inflation expectations more closely. We do not see TIPS as an attractive investment, but rather as an effective hedge and vehicle for return of real capital.

Long duration zeros

This is the ultimate hedge against Armageddon, avalanche caused by the single and unknowable snowflake. Again, we’re not quite ready for that tin foil hat… Absent near term progress on systemic risk and the other big 4 items, our interest may increase.

Equities

Our view is largely unchanged. While it is true that government will likely continue its drive to distort capital flows into value destroying politically driven outcomes, domestic equities represent the only option where the incentive systems drive value producing outcomes. The global Fortune 1000 companies are in the main in pretty solid shape: management, systems, balance sheets, liquidity, and supply chains are as good as we’ve seen them in recent decades. They can weather a significant storm; are in good shape for low/no growth scenario; and offer upside in a modestly stable & growing economy. Below the Dow in red and non-US equities in blue (via Vanguard's All World x US ETF ticker:VEU).

There is nothing new or surprising in Europe & other developed markets, although one suspects we should reclassify Europe as an emerging or regressive economy. Japan is it’s own story, and they’re in the process of reviving economic seppuku. Like your alcoholic relative, Europe continues to sneak in one last drink serially claiming he will stop tomorrow. Not likely. The sovereign emperors and banks have insufficient capital, human, financial or otherwise, and until those houses are put in order things won’t change. You do have some slow rate of positive reaction driven primarily by Germany. On the corporate side, however, we think the major European corporates share most of the same healthy virtues of their global counterparts and should not be disregarded. In the main they play in the same global markets. Sideways for now.

Here is the take away: it always comes back to asset allocation, risk and portfolio discipline. The mechanics of a long term strategy of asset allocation that starts with risk tolerance and includes rebalancing, creates the discipline to buy low, sell high. We believe anyone who ignores those elements does so at his own risk.

Lastly, for all our ranting about systemic risk, we are, and the country should be, grateful to Prof. John Cochrane for publishing Stopping Bank Crises Before They Start just as we were writing, or righting as may be, this piece. He presents an effective solution to our most important economic problem. He's got it right.

hb

hb

"Investors and financial institutions are still accepting significant risks in order to enhance the yield on their portfolios by buying low-quality corporate bonds, holding longer-term bonds, making covenant-light loans that increase the risk to lenders by imposing fewer restrictions on borrowers. They are also bidding up prices of agricultural land and other assets.

The danger of mispricing risk is that there is no way out without investors taking losses. And the longer the process continues, the bigger those losses could be. That's why the Fed should start tapering this summer before financial market distortions become even more damaging." - Martin Feldstein

hb

Washington's $279 Billion Fraud - the unsustainable destructive game just continues.

hb

Wall Street veteran Jim Rickards believes any problems the Reserve Bank has in trying to stave off a recession are its own fault. He also thinks the US Federal Reserve's talk of winding back Quantitative Easing will prove to be just that, talk.

Reader Comments