The taper of Q3: actual results may vary

.

Now you see me, now you don't. Now you see me, soon you won't!

The country seems to be facing a crisis of confidence that now surpasses that of Jimmy Carter’s “malaise”. There is a loss of confidence in leaders and institutions that now encompasses civil, cultural, educational, economic, and Constitutional dimensions. Americans are a practical people: they expect things and people to work, including their leadership.

Consider the non-stop headlines, some small, some large, all cumulatively indicia of a mechanic of dysfunction of large magnitude. It has financial implications.

Let’s start with the Fed, and we’ll quote our last posting which reflects our continuing view:

“We believe the Fed is in fact looking for an unwind strategy but can't find one. A financial Burdian's Ass? Does any bale of hay contain an acceptable unwind? We've gotten a whiff of the revolt of the rational market investors squaring off on the 10 year rates at any sign of tapering which was not pretty.

Our take is that the Fed will do nothing intemperate, take an agonizingly slow incremental approach ... at least while all the knots hold. By this we mean near stasis. We suspect the probabilities are growing for a much longer & slower unwind than many contemplate. We are, however, unwilling to bet much of the ranch on it. The stasis scenario provides 'flexibility' for a strategy that is pinned to the hope of economic growth that may or may not materialize. One is tempted to suggest decades and for the intermediate period a near permanent increase in the money supply. Just a thought. Watch money velocity.” - THE FED, COLLATERAL AND REPO: MORE SYSTEMIC RISK?

The Fed, in pursuit of “transparency”, led the market to anticipate a “tapering” this week, or so some 67% of economists thought. After months of preparation & indications that “we will taper”, they did not. Hmmm.

“Federal Reserve officials created new uncertainty about how much farther they will push their easy-money policies—and new questions about how effective they are at communicating their thinking—with the decision to stand pat on the pace of their bond purchases for now.” Fed's Guidance Questioned As Market Misreads Signals

Paradoxically, the Fed is adding uncertainty as to the predictability of its short term actions but more certainty as to the ultimate outcome of its strategy. QE and the balance sheet of the Fed, which is now the largest undercapitalized hedge fund in the world, will have to be downsized, unwound at some point. The inflated asset prices it has created are not sustainable nor is the continual expansion of the money supply nor is the balance sheet of the Fed without market constraint. OK, but some problems arise. We don’t know the timing, magnitude, consistency, or forms of the ultimate unwind or market response. We do know that large complex things take time to process and adjust (or as the dinosaurs, die). We do not know the form of market response as it will be influenced by mode & timing of implementation. Intuitively, we see two polar options: a potentially chaotic repricing of some magnitude or a gradual decline of our standard of living induced by inflation and/or lower productive economic output over time. Likely, it will be a more moderate combination of both. It is a huge Markov Chain. Look for rising risk premia.

One thing is certain: no jobs means no recovery, no growth. U6 is the green line. We basically have 15% of the country out of work. Equally disturbing is the youth unemployment: we are loosing a generation of workers which has huge long term cultural & economic implications. These wheels grind slowly but finely, and the fate of the black nuclear family comes to mind. The Civilian Unemployment rate is simply misleading & does not count those who have left the labor pool over time for want of employment.

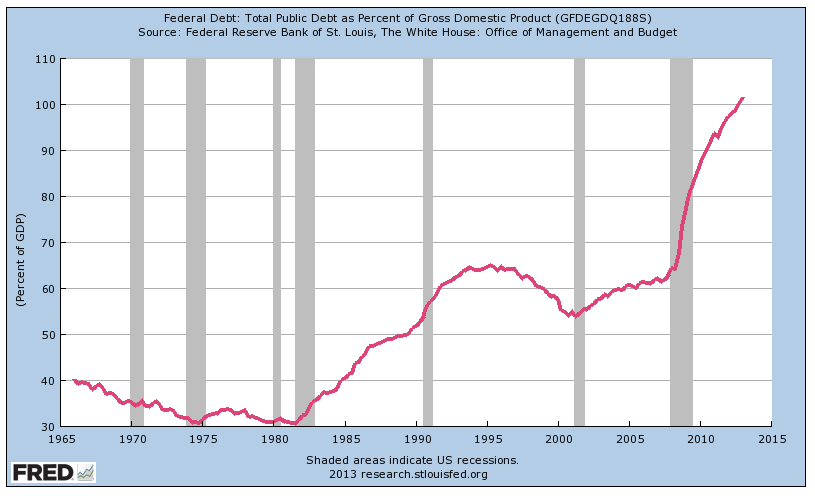

As to the inevitability of outcome consider this and ask if the trajectory is sustainable. Recall it omits unfunded liabilities:

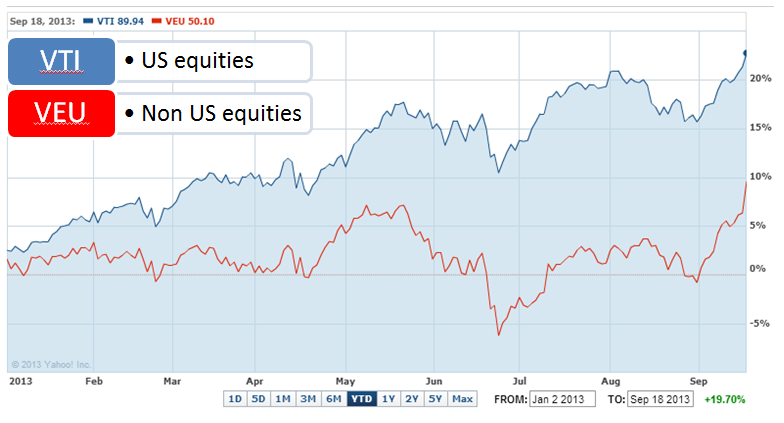

Equities: But the juice works in the short term. Set aside for a moment that steady decline in real median family income and take a look at the ride in equities: Obama and Bernanke have delivered for the 1% like nobody's business.

US and non-US equities have put up great numbers. It seems extended low growth with expectations for the grind to continue in the US has been sufficient to buy Euroland and Asia some time to put their houses in semi-order. We remain skeptical of expectations for higher growth in the US. Evidently, so does Mr. Ben.

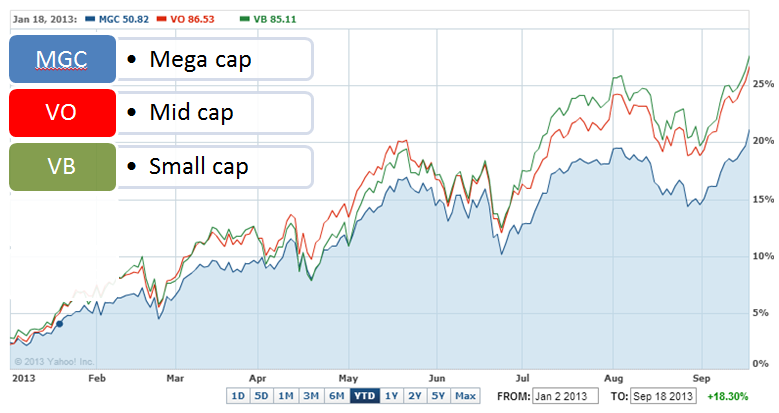

Large, mid and small caps all up: beta wins. These are outsized gains clustered within a relatively small time frame.

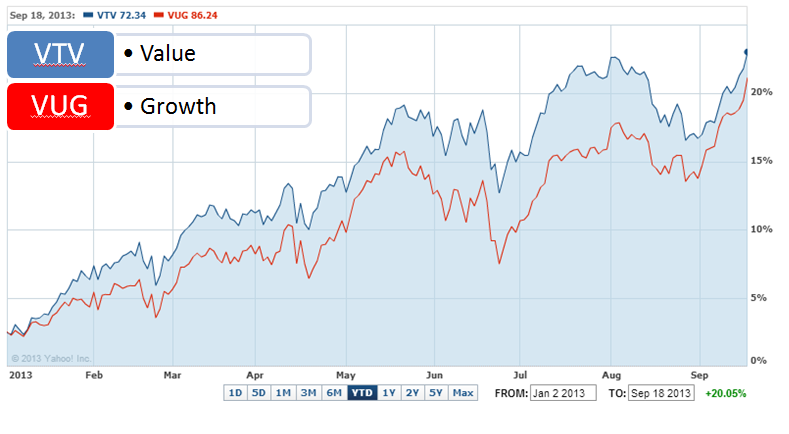

Growth or value pretty much didn't matter.

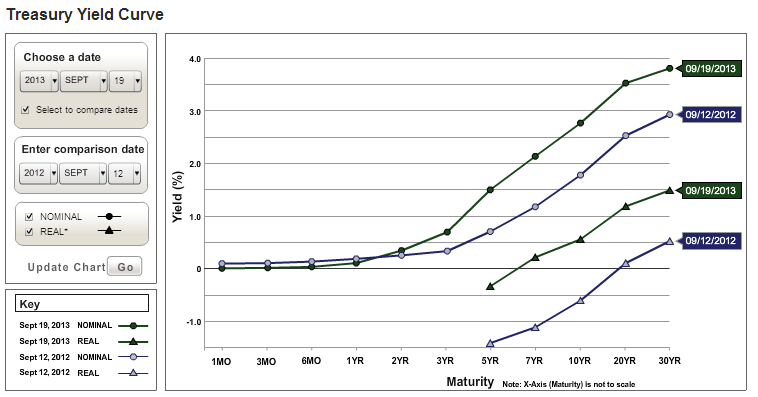

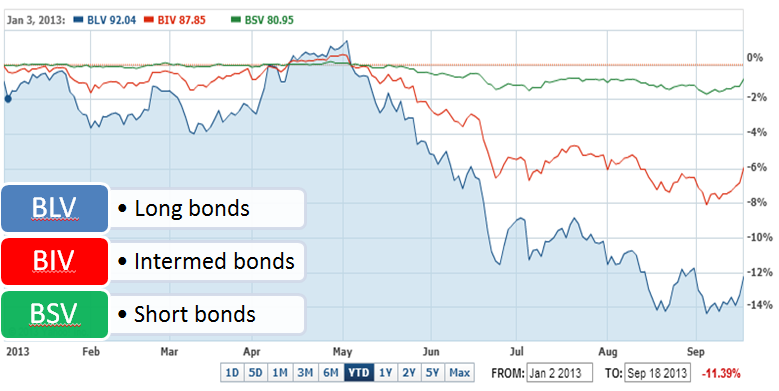

Fixed income: we know too well the implications for continued manipulation of zero to negative real interest rates. It is a coersed wealth transfer from savers & risk constrained investors to borrowers. You get no or negative real return on your fixed income investments, and the borrowers (including the US government) get the interest you do not. It’s pretty simple. In a macro perspective every fixed income investor (from Grandma to Bill Gross) become poorer. Real rates have increased substantially in proportional terms, and we suspect more to come... when is the question.

Meanwhile fixed income investors have learned a harsh lesson: maybe Grandma shouldn't hang out in long bonds. More learning to come?

We note again there are only three ways to get yield in fixed income: duration, credit risk, or liquidity risk. As the Fed starves the market of real interest rates, it drives investors out the risk curve along any of those parameters. So, if you buy the thesis that the current game is not sustainable, do you load up on duration, credit or liquidity risk when you know the markets are distorted by the Fed at the precise time when the Fed has demonstrated you cannot rely on its indications of policy? We think not, unless you have impeccable market timing which, by the way, neither you nor we have.

We maintain our bias to short duration investment grade product. A diversified portfolio with a duration of 2.7 pays a spread of .97% over the interpolated Treasury rate. Consider that the 3 year Treasury currently pays .87%. The credit spread is more than the underlying Treasury, not a bad value. We caution against chasing yield: it never ends well. You just can’t get 8% in a 2.75% market. Remember that next time PT Barnum starts pitching you.

Our outlook: We anticipate low growth and increasing risk premia induced by the Fed, ill conceived regulations or geostrategic blundering. We look for sluggish employment and weak capital expenditures. Every dimension of fiscal, monetary, social, energy & tax policy is directionally wrong from an economic perspective. Paralysis may be the best hope as a least-worst outcome. We anticipate Ms. Yellen will be the nominee to head up the Fed and do not anticipate that she will raise rates in face of a congressional election year and certainly not in a presidential cycle, but as they say, the opera isn't over until the fat lady sings.

Stocks and bonds will respond favorably as will all risk assets. Everyone may well join the drunken pig pile, and all the animals of the forest will be happy, at least for a while. Systemic risk & moral hazard will grow and long tailed risk will increase. We see near term risk of inflation as offset to some extent by slack capacity in the economy.

For equities the good news is that globally corporate balance sheets continue to be in great shape (excluding financials) and well positioned for marginally decent earnings in a slow growth environment. There is much less opportunity for cost cutting & greater efficiency. Earnings growth will start to converge with nominal GDP growth.

It is no trivial matter for the asset class as a whole that corporate compensation models are much better aligned toward wealth creation. There is no such scheme with fixed income assets, save the anti-model of governments that are driven by grafted re-distributionism, so to speak, and incentives to inflate. Equities historically have been a source of high sustainable real returns, and we don't anticipate that will change. We do anticipate greater uncertainty which may manifest itself in greater volatility from here to there and stretch the time frames required for those expected returns to eventuate as business models adjust.

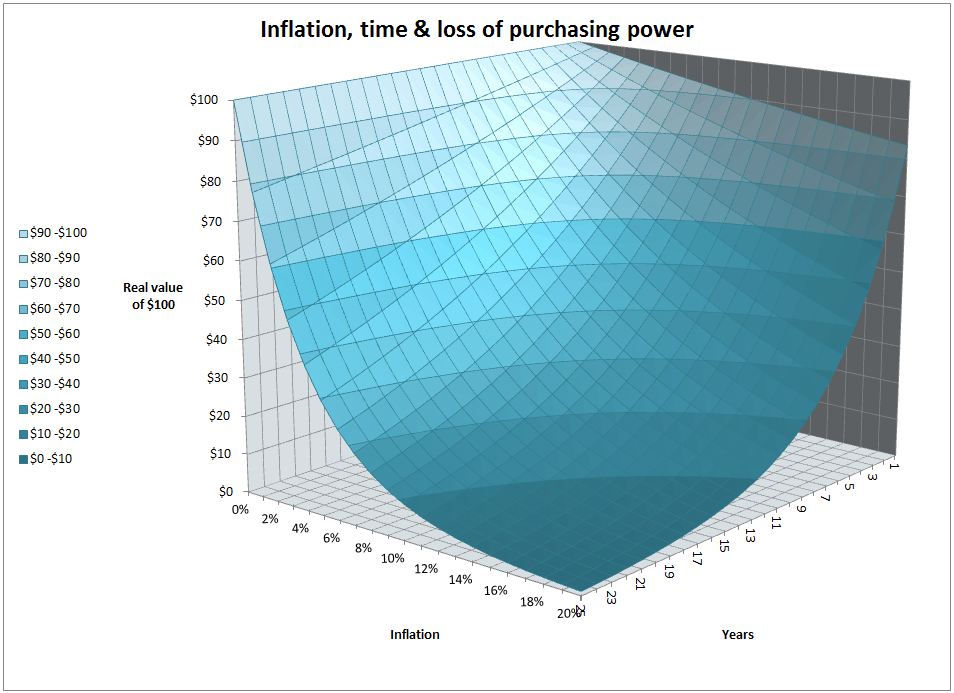

We'll close with two last comments. We see two major risks to long term investors. One takes the form of undisciplined investment programs that devolve to decisions driven by emotion which in turn subverts the asset allocation and risk management. The fog of uncertainty holds implications, again, for the importance of asset allocation and diversification. The other risk is inflation. If you think you can go to cash and sit this out, consider the picture below (reproduced from PRE Q3: IT'S NOT AN EMPTY CHAIR, IT'S AN EMPTY WALLET). Here's a hint: if the graph starts to get darker blue, you've probably lost 70% of your real value.

hb

hb{kind=link}

Reader Comments