Q2 2015 Commentary: the pruning knife vs two issues

Our market outlook is simple. Nothing will happen between now and November 8, 2016, that is, nothing particularly good. Anticipate no reform of policy or regulations... tax, fiscal, monetary, environmental, energy, labor, or educational matters. We may see futile, symbolic, political gestures, and we will most certainly see Obama launch a last wave of initiatives, mostly by Presidential fiat, and some will likely be materially destructive. A cynic might argue Republicans have incentive to let them roll, to sit and watch the rubble in advance of the elections. But who among us would be a cynic?

Meanwhile the big economic picture remains the same. Our national problems remain unsolved, and so they compound, become more deeply embedded, more complex & costly to remedy. There seems to be another broad phenomena, coincident or causal: everything seems more brittle. We have previously, some would say endlessly, pointed out our concerns about systemic risk, flawed regulations, flawed incentives, and structural concerns with our markets & economy ... but this notion of brittleness extends well beyond the markets. It seems to have extended deeply into our culture, our confidence in leadership, our social fabric, rule of law, civil discourse, race relations... you name it. Brittle things break more easily.

There are such things as bad endings, and they have severe consequences: Detroit or Puerto Rico or Greece. Europe’s debt crisis is much broader than Greece, but less publicized as the fuse is longer.

“Italian total real economy debt (government, household and business) is about 259 per cent of gross domestic product, up 55 per cent since 2007. France’s equivalent debt is about 280 per cent of GDP, up 66 per cent since 2007. This ignores unfunded pension and healthcare obligations as well as contingent commitments to eurozone bailouts.

Italy is running a budget deficit of 2.9 per cent. Government debt is around €2.1tn, or 132 per cent of GDP. French public debt is just above €2tn, or 95 per cent of GDP. The current budget deficit is 4.2 per cent of GDP. France’s budget has not been balanced in any single year since 1974

Italy’s economy has shrunk about 10 per cent since 2007, as the country endured a triple-dip recession. Italy’s unemployment is more than 12 per cent, with youth unemployment about 44 per cent. French GDP growth is anaemic, with unemployment above 10 per cent and youth unemployment of more than 25 per cent.” Source: http://on.ft.com/1KbJ6at

And for all the sound and fury, nothing has been fixed in Greece. It will go on endlessly with further adjustments, additions and right sizings. Greece will devolve to a near Third World living standards.

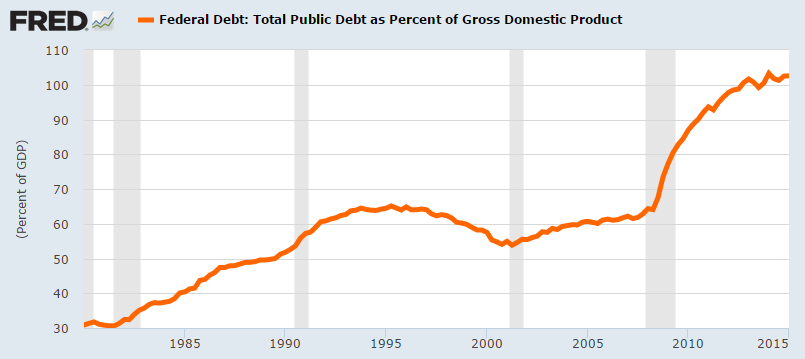

We have our own growing federal debt & unfunded liability crisis, and we better pay attention.

The graph above is simply funded debt and does not include unfunded federal liabilities. The distinction is important. Funded debt is evidenced by a bond or note and is recorded as debt on the government’s balance sheet. Unfunded liabilities are ‘promises’ not evidenced by a note or bond and not recorded as debt on the balance sheet of the government. Unfunded liabilities such as pensions, Social Security, ObamaCare, other healthcare, or hidden, unfunded obligations, dwarf the actual and reported funded debt. This we know as the fraud of government accounting. These unfunded obligations are equally important in a social and economic context as the funded debt.

As Stanley Druckenmiller has noted, the ballooning costs of Social Security, Medicare and Medicaid (which with unfunded liabilities estimated as high as $211 trillion or about 12x the actual funded federal debt,) will bankrupt the nation's youth and pose a much greater danger than the debt currently being debated, much less understood, in Congress.

Recall Detroit, Chicago, Harrisburg, Stockton, Puerto Rico? Consider that pension expenses now consume some 18% of Chicago’s entire annual budget. They’re cooked, like Puerto Rico. Here’s one list of the body count and another of the next 20 to go.

We have low growth and falling productivity, and there is no short term fix. This is a structural problem created by misguided policy. Productivity is the most important metric of the economy. It is how we sustain and grow our standard of living.

“Productivity over the past six months fell by the most in more than two decades, leading to increases in U.S. labor costs that threaten corporate profits.The measure of employee output per hour decreased at a 1.9 percent annualized rate after a revised 2.1 percent drop in the prior three months, a Labor Department report showed Wednesday in Washington. The decline on average over the past two quarters was the biggest since the first six months of 1993.”

Biggest U.S. Productivity Drop in Decades Sends Ugly Omen May 6, 2015

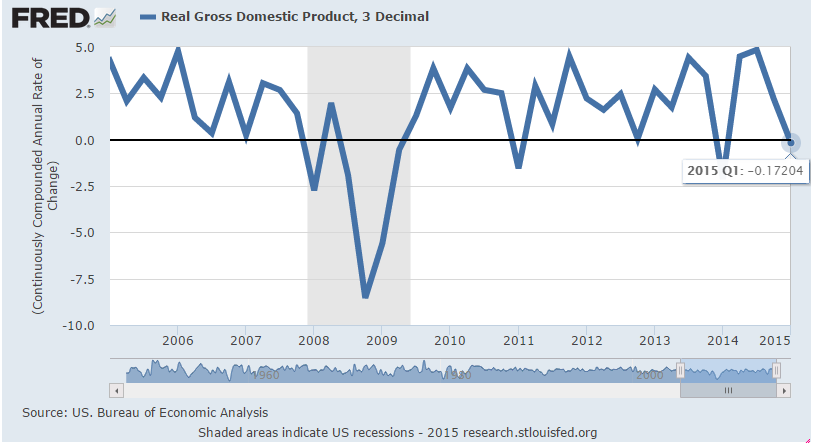

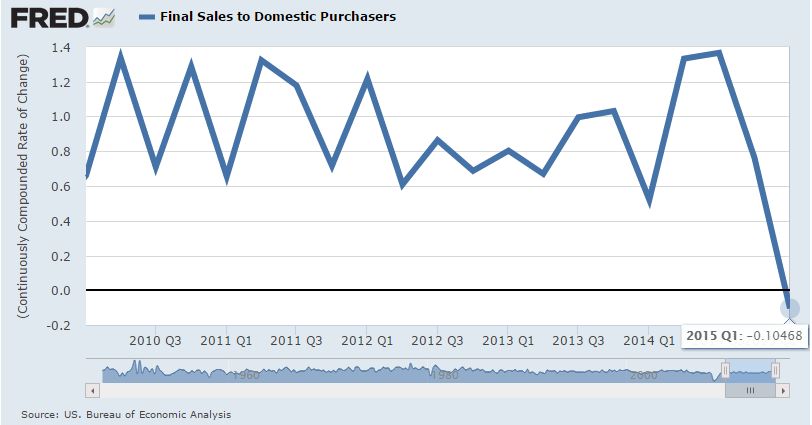

Real GDP growth remains weak and erratic, as do Final Sales to Domestic Purchasers, another indicator of economic activity.

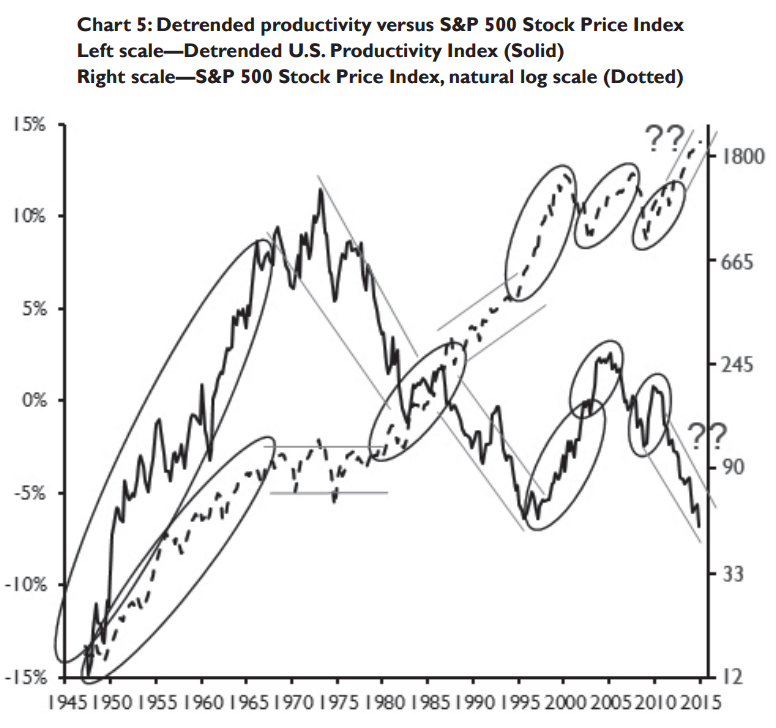

Want to get really ugly? Look at Jim Paulsen’s chart from his June 19th commentary: see the solid line, left scale for productivity.

Note the trend of decreasing productivity and the negative correlation to stock prices. Perhaps a temporary and reversible consequence of fiscal excess & easy monetary policy? A colleague asked what detrended means. It’s a high level geek process to wash out autocorrelation & “memory” of data sets. Good luck.

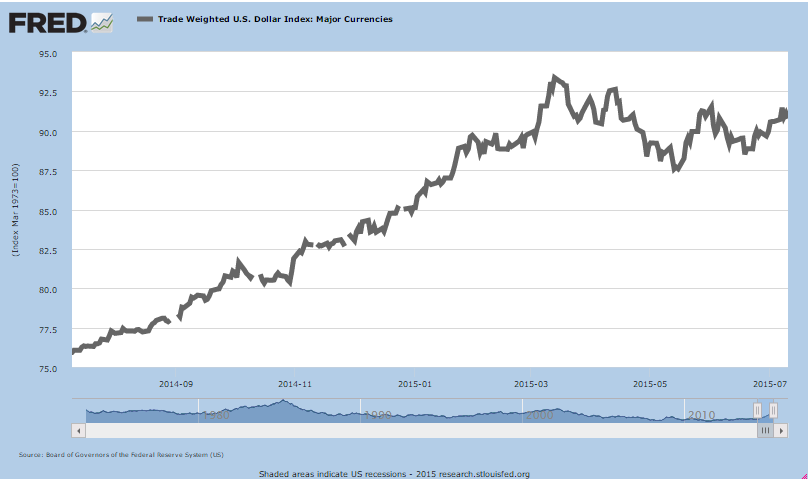

We have a surging US$

The trade weighted US$ is up about 20% over a one year period. This makes it a tough for domestic companies to export, but very cheap to import. Other than that we’re not sure what impact this will have. Clearly it’s adversely impacted the USD$ value of unhedged foreign currency debt & operating cash flows. May we suggest this would be a good time to travel abroad? Perhaps to buy low: vin rouge, pommes frites or foreign stocks, anyone?

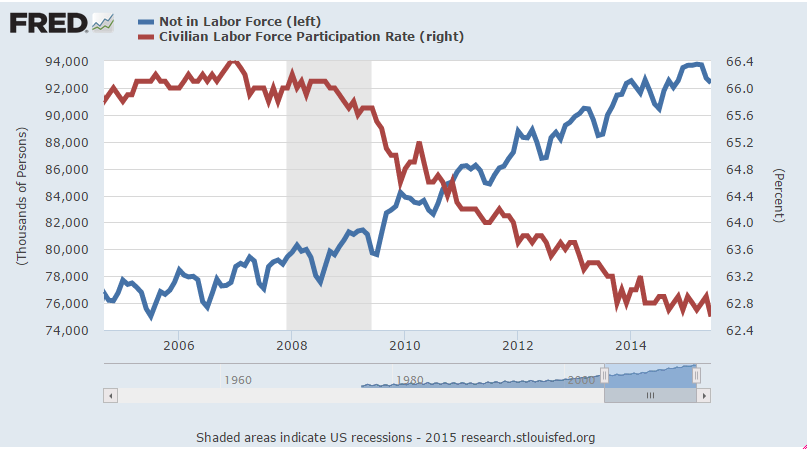

We have record low labor participation rates: more people in the cart, fewer people pulling it. This is an extended trend with no improvement, no fix in sight.

“the labour force participation rate stands at its lowest since the 1970s, suggesting millions of people remain on the sidelines of the jobs market rather than seeking or holding work. The question is whether this decline in the active workforce is largely a structural one — related, for example, to an ageing population — or a cyclical one that could be countered with stimulative monetary policy.” http://www.ft.com/intl/cms/s/0/72759f3c-2a35-11e5-8613-e7aedbb7bdb7.html#ixzz3fxR4mroa

We think the answer is obvious. Demographic cycles can influence these numbers, but ‘stimulative monetary policy’ does not work when the stimulus is consumed (by wealth transfers) rather than productively invested. Our problem is structural, manufactured by policy, and subsidized to that form. We need productive labor and investment.

Our take going forward

We look for slow to low growth to continue with no particular change in trend. We anticipate the Fed, having boxed itself into a corner, will raise short term rates modestly in late Q3 unless the economy completely stalls, We do note the allegations of the Fed leaking material inside information which is a non-trivial distraction.

We expect a modest rise of .25% will be benign to equity markets. Given continuing chaos in Europe, weakness in Asia & the emerging markets, and the massive flight money coming into the US dollar, we don’t see the long end of the US$ interest rate curve moving too much. Longer rates could actually go down given weak domestic demand. We could be wrong, and we’re still averse, but less so, to extending duration right now. We still like short term investment grade product as a relatively safe harbor.

We anticipate lower or stable energy prices but the benefit of that reduction will be consumed again by tax and cost increases of ObamaCare, and the consumer will continue to be squeezed. It’s hard to imagine the magnitude of burden our new health care system is placing on citizens, but there it is: The Coming Shock in Health-Care Cost Increases, right in the WSJ. We don’t see how the consumer is going to be having a good time, and this will ultimately reduce corporate top lines and capital investment. It already has, and this too will continue.

So, it’s sideways, low, and slow to the election. The equity markets will be relying on the remarkable efficiency and resiliency of corporate America, well placed with good liquidity and strong balance sheets, to make adequate profits with 1-2% real economic growth. For sake of clarity, we’re not jumping out windows here.

Our major concern: life goes on after the election. The big problems are unresolved and in the main getting bigger, and it is imperative we get a timely, sober, and practical grip on them. We’re running out of rope, and it’s in the markets. We anticipate lower returns in equity and fixed income. It will take some time to wash out the sand in the gears.

“Many investments today using artificially cheap capital are not increasing productivity — they are being made because money is cheap and the profit motive is strong. Consider the evidence. This year likely will witness record US stock buybacks; the second biggest year for mergers and acquisitions; the highest percentage of non-investment grade borrowers among new issuers of corporate debt; and a record for covenant-light loan issuance.” Source: http://www.ft.com/cms/s/0/8c860c72-23d7-11e5-bd83-71cb60e8f08c.html#ixzz3fxNSO6Fm

We all know we’re waiting for relief. We’re at the front end of a period change, the direction of which is unknown. In the meantime we have seemingly a national crisis of faith, suffer from poor leadership, and, we believe, destructive policies. Markets, healthy economies, and stable democracies require sensible policies with stability & predictability of rule of law. Rising standards of living require freedom and incentives to innovate. For now we seem to be losing them ... unless you can buy ‘em from politicians.

That’s the problem. The good news is that it is not too late. The bad news is that we can little afford to keep ignoring the problems. Greece happens.

###

"The pruning knife of taxation is a very important instrument. With it the workers’ state will be able to clip the young plant of capitalism, lest it thrive too luxuriously.” - Leon Trotsky

“As long as it is admitted that the law may be diverted from its true purpose — that it may violate property instead of protecting it — then everyone will want to participate in making the law, either to protect himself against plunder or to use it for plunder. Political questions will always be prejudicial, dominant, and all-absorbing. There will be fighting at the door of the Legislative Palace, and the struggle within will be no less furious. To know this, it is hardly necessary to examine what transpires in the French and English legislatures; merely to understand the issue is to know the answer.

Is there any need to offer proof that this odious perversion of the law is a perpetual source of hatred and discord; that it tends to destroy society itself? If such proof is needed, look at the United States [in 1850]. There is no country in the world where the law is kept more within its proper domain: the protection of every person's liberty and property. As a consequence of this, there appears to be no country in the world where the social order rests on a firmer foundation. But even in the United States, there are two issues — and only two — that have always endangered the public peace.” - Frederick Bastiat in The Law, Perverted Law Causes Conflict, 1850

hb

hb

If you're looking for a good primer on pension liabilities and accounting try:

Staying Afloat in a Sea of Pension Numbers

hb

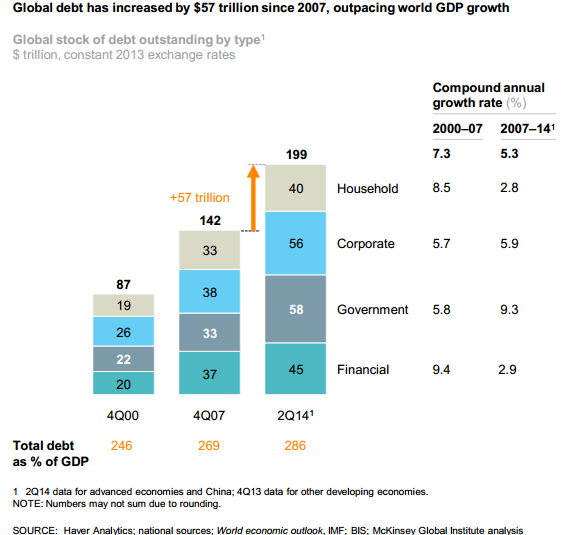

Here is the Debt and (not much) deleveraging study by McKinsey of Feb 2015. It is worth a look. Surprisingly, it takes a pass on the issue of unfunded liabilities.

Reader Comments