A look at the markets: a brand new day?

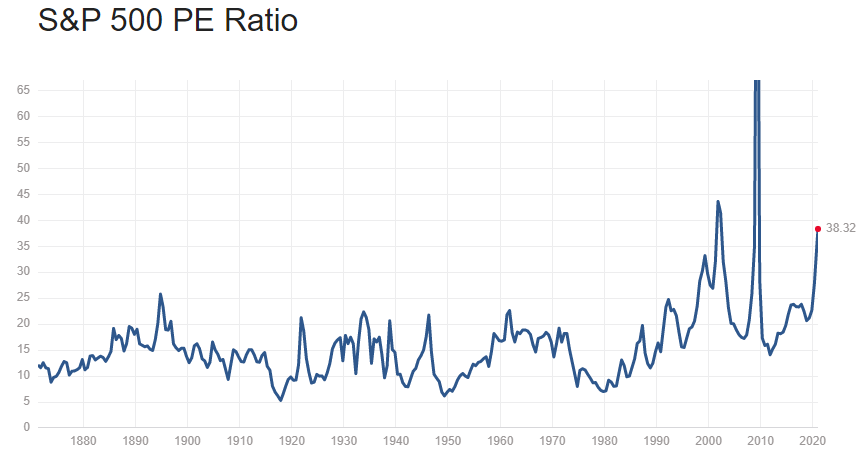

US Equity markets: overvalued by most historical standards. Pick your preference.

Source: a/o 1/21/2021 https://www.multpl.com/s-p-500-pe-ratio

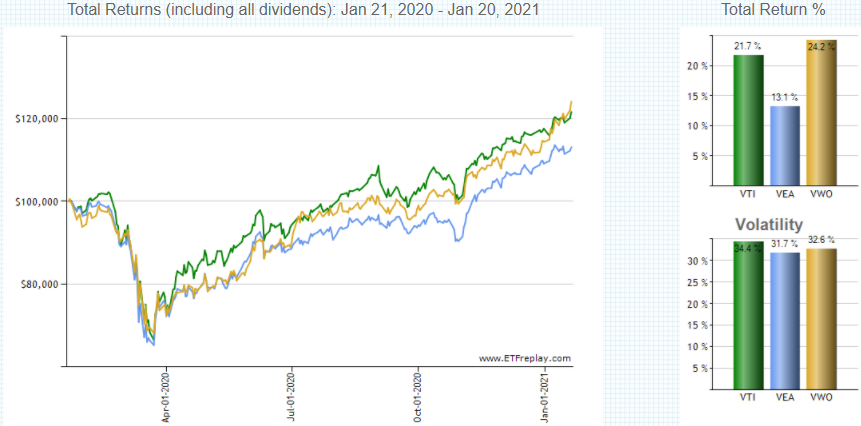

Realized returns: the recent performance of equity markets globally seems to be completely out of synch with the real economy. Fine. We get repricing to the long view of value, but we also get the Fed juicing the markets like old race horses in Kentucky. We view the current levels with caution.

Below we see the realized compound annual rates of return since March 23, 2020, to Jan 6, 2021. The Vanguard Total US Market appears in green; the Vanguard FTSE Developed Ex North America (foreign developed markets) is in blue; and Vanguard’s FTSE Emerging Markets in gold. They are supra normal returns, in our opinion, and place us at unsustainable price levels. The bid comes from the output of MMT: money has to go somewhere and fixed income presents it’s own special problems (see below). The problem with equity valuations is simple: they’re high and fragile with respect to real productivity, and they don’t have to stay there.

Source: https://www.etfreplay.com/charts.aspx

US fixed income markets & rates

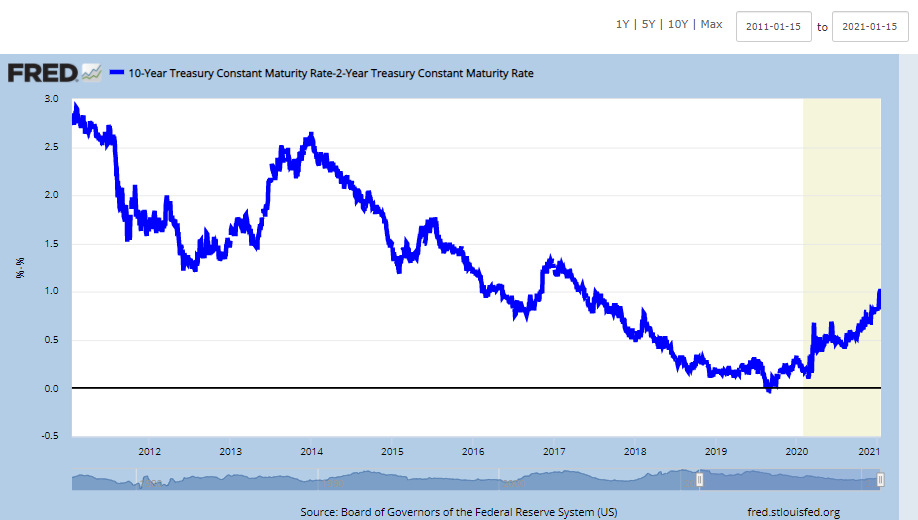

10 & 2 year Treasury rates: the 10 yr shows upwards pressure and fixed income portfolios could be at risk in face of further increases. Why buy negative real rates loaded with duration and run by reckless or feckless, as you like, governance that is continually increasing it’s risk profile? Could the bid for Treasuries really back up? Yes, fast and hard, as we’ve seen before (c.f. Taleb on fragility and chaotic behavior of non-linear systems which translates in plainspeak to a string of obscenities followed by ‘no bid’). We do know these things can happen but we don’t know which snowflake might cause an avalanche. Neither does the Fed.

10 year less 2 year Treasury yields gives a better look at the upwards pressure:

Treasury Real Yield Curve Rates: real rates are negative across the yield curve and have been for a while. To the younger generation and pensioners: try to retire on these. Inflation, by most measures is positive. To corporate and sovereign borrows: investors will pay you to “borrow”, so back up the truck and enjoy the subsidy from investors. Oh, and same to home owners. Leverage, baby, put the pedal to the metal. MMT makes it free. Well, perhaps more on that later.

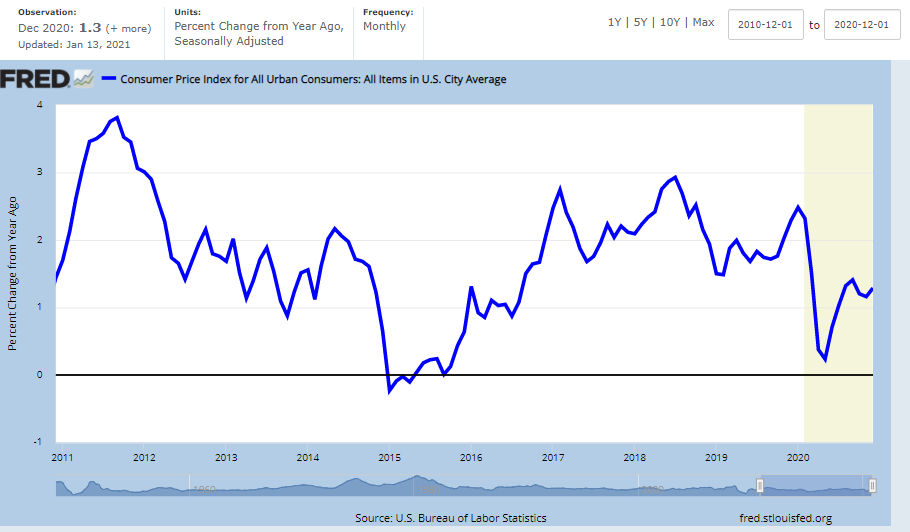

Inflation:

CPI, % change from year ago

Forward 5, 5 year inflation rate (the expected inflation rate 5 years out, for the next 5 years). Ok, so if the market is expecting inflation of, on average, 2%+ in that timeframe, why would you buy a nominal 10 yr Treasury today at ~1.1%? Go figure.

Probabilities of Fed targets: a lot of blue paint below (indicating no change) on this one, as far as the eye can see, which one suspects in current conditions is not very far at all.

Source: https://www.cmegroup.com/trading/interest-rates/countdown-to-fomc.html

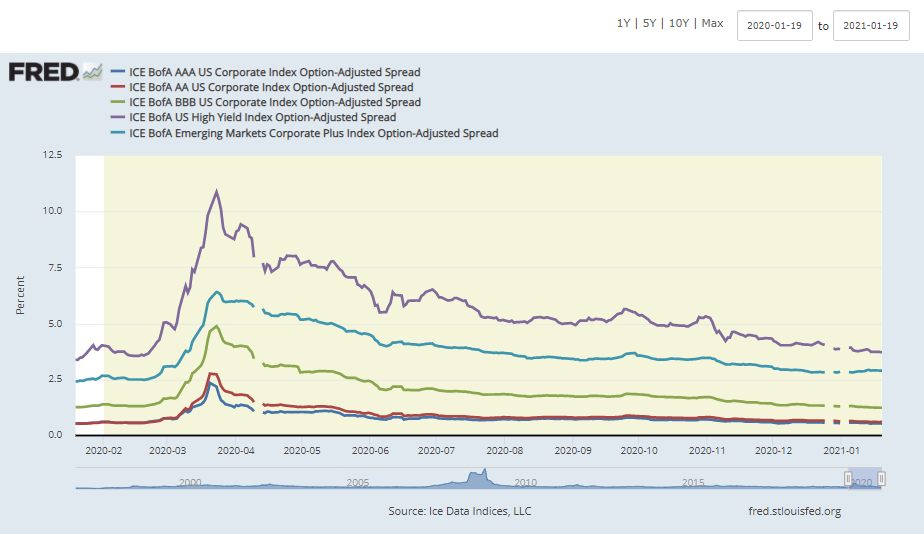

Credit spreads: bear in mind the Fed has been buying credit products, including many of the largest junk & investment grade bond funds, and you can see the dramatic impact it had. We think it’s bad policy whether in the fixed income or equity markets. Investors need price discovery and it is now impaired.

Now think about what happens if the US$ weakens and rates rise. Will you wake up and learn the Fed kicked the crutch out from under the market? That might be an ugly too late. See the problem? Fear of and reliance on the Fed.

Our only observation is that it’s hard to know how much of the decline in spreads is synthetically driven by the Fed, but even so, a curated (for credit risk) portfolio of short duration investment grade bonds does offer a credit spread well in excess of the 10 year Treasury, maybe even a modest, though positive real return. Who knows? To be clear, this is not a investment recommendation: nothing here is.

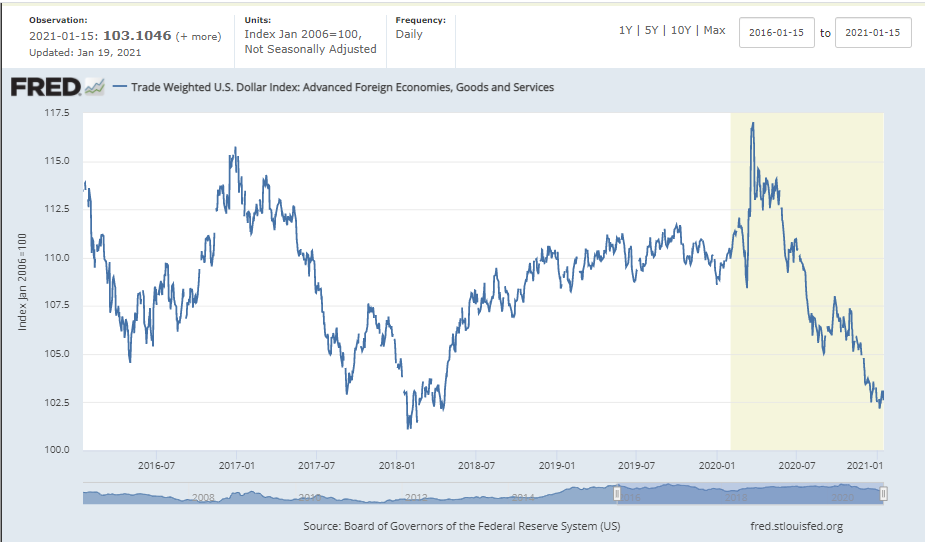

US$ trade weighted vs advanced foreign economies: dropping like a rock.

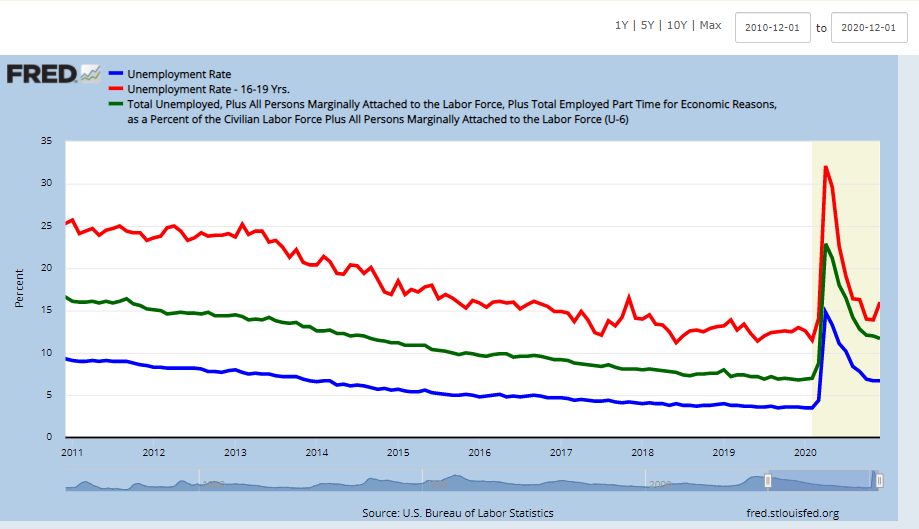

Labor markets

Unemployment: still weak, but recovering. Youth unemployment peaked at ~ 32% in April of last year. Brutal numbers over the last year, but the rate of recovery was, and hopefully remains, relatively robust, if not improved by the advent of vaccines. The outlook is unclear at best.

Labor force participation: brutal. Look at the blue line Not in Labor Force.

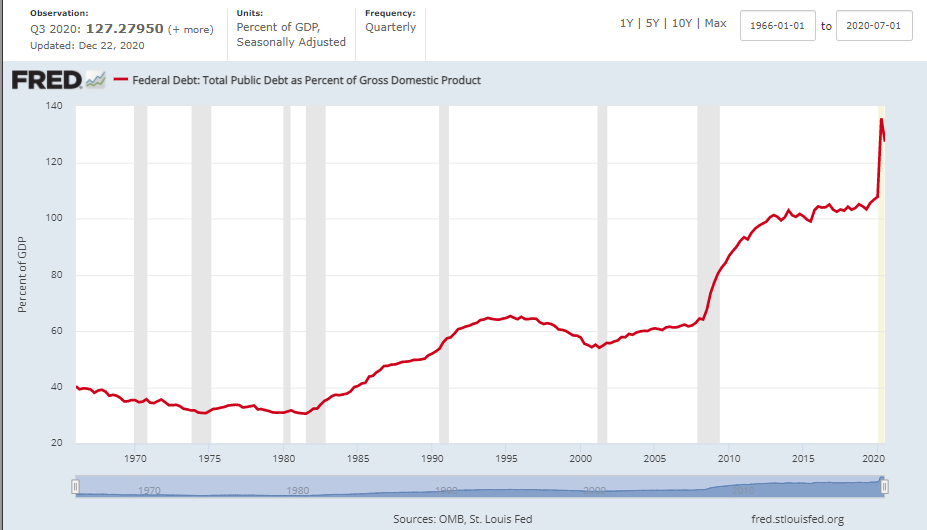

Federal debt as % of GDP: read ‘em and weep. We hit the highwater mark of ~136% and that maintained likely by some very fancy bookkeeping. And we bear in mind that Federal debt is only a minor component of our debt problem as unfunded liabilities at all levels of government make these numbers look like small potatoes. We are in process of a massive liability transfer to the next generations. In our view this is financial gross negligence, and we refer you to The Grumpy Economist, John Cochrane for a more fulsome explication of the risks. In our opinion MMT is a destructive and dangerous fairy tale of a Big Free Lunch.

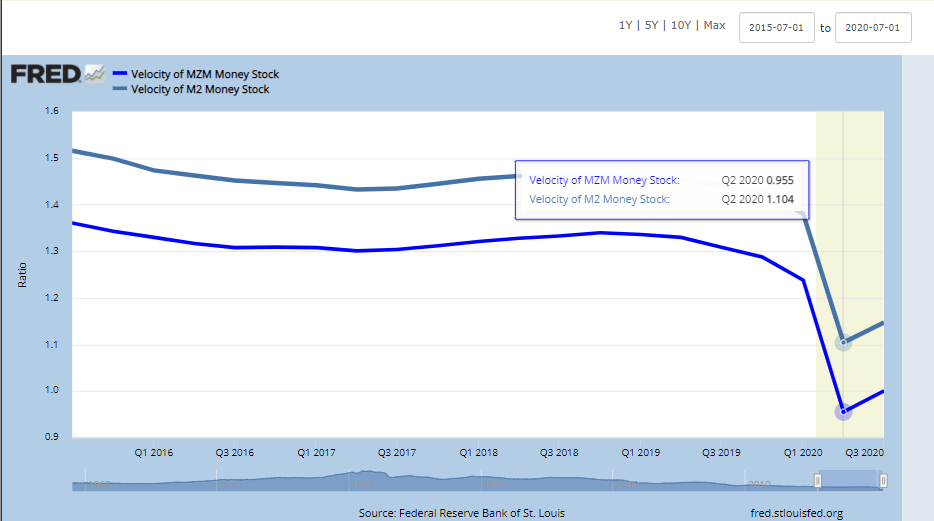

Velocity of money: Note the slight uptick starting in Q3. This is a positive sign indicating some recovery, but also realize this is a backwards looking view, significantly lagged. The changes on the margin occur very quickly and are translated instantaneously to global pricing of the rate markets. So if we’re printing MMT money, and demand for money increases, one might envision the arrival of material inflation quite quickly, such that you read about it after it happens.

Summary

In many ways this is a rehash of many of the issues we’ve raised in prior commentaries, but it’s a little different in that everything more cachetic, more leveraged with less capital, institutionalized & ossified while the degrees of flexibility accorded policymakers are getting limited. The window for sensible incremental changes seems to be closing slowly over time which provides, akin to a gambler in a poker game with fewer and fewer chips, greater incentives to go all in. MMT and the Great Green Subsidy come immediately to mind and media. Initiatives to raise real productivity do not.

We see overvaluation in both equity and bond markets. If so, a consequence may likely be the loss of the traditional view of bonds as having significant diversification value relative to equities. which is a very big deal to portfolio construction. If inflation & rates head north, then the traditional 60/40 portfolio of equity/fixed income may get a load of bird or buck shot, both barrels.

We also observe the level of faith by federal policy makers, and we mean precisely that word, now exceeds that of what few snake handling preachers seem to remain. The new budget and regulatory priorities to us seem to be fraught with opportunity for more rent seeking and mal-investment while the Fed’s MMT provides the framework to fund all of it, along with the mass of leveraged zombie companies who can survive only by grace of the low-to-no-to negative rate structure with the Fed at the window with a bid.

The option to induce real economic productivity and grow the economy to mitigate the debt threat may work, but let’s recognize that contrary to the assumptions of Glorious Outcomes, the incremental juice to productivity in response to massive government spending can actually decline. In fact, it can go negative. There are such things as negative multipliers. The private sector will likely face higher taxes and more regulation hence less incentive on top of less capacity to make large scale investments given current uncertainty.

So what to do? Diversify. Ok but into what? Frankly, we don’t have an answer we’re confident in except for this: we're cautious about viewing the bond market, particularly longer duration, as a less risky asset. And we’re well past viewing US Treasuries as a risk free asset although we hope the world does not join us in that view. Perhaps Grandma should rethink longer duration and higher risk corporate spread product? How about a credit spectrum running from a minimum of high quality investment grade to Treasuries? And no structured stuff. Keep it simple.

We do have a thought born of our cognitive limitation and desperation: consider broadly the incentives which impact different forms of governance, for example corporate vs government. On a sober day we know neither is particularly your friend, but which knows how to make things better, faster, cheaper? And which is incented, gets paid to make it so?

The Fed, Congress or CEO’s and the boards they report to?

hb

hb

Reader Comments