What has changed with the new debt deal?

In the debt deal we had a large scale and global demonstration that there is a fundamental, costly, and cumulative flaw in the governance process of the US. One suspects that very few people actually understand the magnitude of the problems of our debt, unfunded liabilities, and increasing macro-economic drag of the costs of regulation.

I don’t buy the notion that the debt ceiling deal is a model of American republican democracy at work. To the contrary: it is emblematic of the problem. We don’t know if we want to be a market economy driven by innovation and freedom or a socialist economy driven by redistribution of wealth.

The markets know that and are just going to hang out and price in, every day, the continuing drag of opportunity cost and inefficiency, until we get the major question sorted out.

As it stands now, citizens shall soon lack even the ability to buy an incandescent light bulb. This, perhaps a small thing, but one that diminishes that Shining City on the Hill.

Won’t it save the AAA ratings? Are AAA ratings important to the US?

Let me answer your question with a question. What was the economic value of the enterprise of the United States three weeks ago? What will it be three weeks from today? The answer to both is about the same as it is today, maybe a bit less, maybe a bit more.

What do we know today that we didn’t know before? Well, we know that Lisa Jackson thinks that under the Clean Air Act "For every $1 we have spent, we have gotten $40 of benefits in return. So you can say what you want about EPA's business sense. We know how to get a return on our investment…" and that this ethos, certainly not logic, remains a driving force behind our national policies that drive capital formation, investment, and employment. There are manifold examples of other continuing policies of the administration that are even more destructive of economic opportunity which we leave to others to explore.

We boldly predict the AAA ratings of the US will not hold because we have too much debt and a decreasing ability and willingness to pay it off. The ratings are largely irrelevant except as an indicator of long term economic & cultural decay. They may be seen as an accumulation of bad policy, bad political decisions rendered by the voters, and poor leadership over time.

We do note that even if we are wrong on the ratings call, we will be right in this ken: recall GM’s paper trading at junk levels in the capital markets while carrying investment grade ratings all around? As a capital markets issue, generally, the rating agencies are irrelevant. They are generally behind the game and even if they understand the credit, which sometimes they don’t. And by the way, aren’t the agencies regulated as deemed systemically important institutions?

The capital markets price credit risk every day. Go look. Last count there were about 65 entities trading better in the markets than the US government. Probably more today.

How will this be fixed?

People will vote in November 2012.

We have to decide whether we want to be a market & innovation driven economy or an economy based on redistribution of declining stocks of wealth. Productive people and capital will decide whether to stay or go elsewhere.

In the meantime the debt will compound, the spending will compound, the demographics of the country will age, domestic capital formation will stagnate, investment will decrease, interest rates will go up (barring another recession), and investors will look for ways to mitigate financial & regulatory oppression.

How will the market be changed by this deal?

I don’t know, but this is one of the few times in modern history when retail and large scale institutional investors may come close to informational parity, largely due to the complete unpredictability of political outcomes, the lack of enforceability of political contracts (will the SOB’s do what they promise?), and the now increasingly valid questions about the sustainability of rule of law in the US.

Try to allocate capital to create wealth in that environment.

Go hire a Wall Street law firm and ask about the certainty of senior secured creditors’ rights in “systemically” important credits, like Chrysler or GM or GE. Or compare the answers to “What do you think about the possibility of something big & bad happening in the markets?” A quant geek will talk about six sigma events, kurtosis and the like, while Joe Everyman will say, “Sure seems more likely”. Which can you take to the bank? And meanwhile, some Wall Street analyst demonstrates complete dis-utility while bleating that XYZ Company is $.01 over expected EPS. No one cares.

No one cares because it does not solve the problem.

Is the debt ceiling deal good thing?

No, not really. In one sense it is very destructive because it perpetuates the language and manner of a continuing fraud on the American people … by that I mean the entire construct of disinformation where by common meaning and reference are inverted and no longer have validity. Disinformation & newspeak are working.

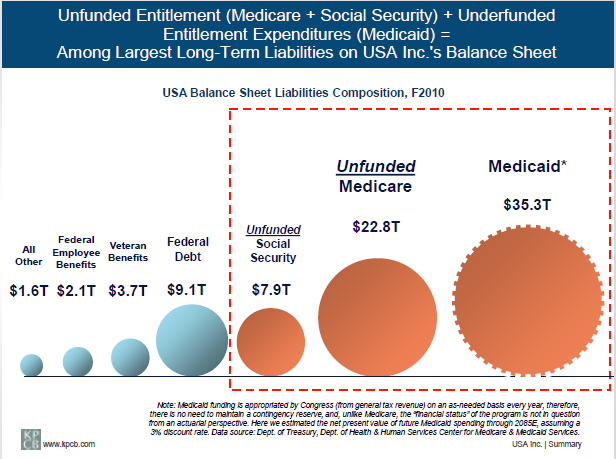

Material liabilities are hidden, off budget, and off balance sheet. Taxes are no longer called taxes, but ‘revenues’ and tax reductions are not tax reductions but ‘tax expenditures’. Reductions are not real reductions but reductions from some fictional abstraction called a Baseline which has no relation to actual spending except to facilitate more of it. Debt limits don’t limit debt, but provide a forum for an increase in debt. "Investments" are not investments, but political allocation of scarce capital resouces away from highest & best use. The government wants to invest in a high speed train, you want to invest in your kid's college education. Your personal priorities as to how you want to allocate your resources count less and less every day. Same with corporations, it just takes a different form.

So we are where our governance has delivered us. No one should be surprised at bad outcomes. Most know that if an entity repeatedly consumes rather than invests, it doesn't work. Or if an entity makes lots of bad, over leveraged investments over time, it doesn't work.

More problematic is that no one believes the process or manner of conduct of the game is effective or reputable anymore. A friend commented “I don’t know what can be done to get these guys into reality”. The reality of the political class is different: they are in the wealth transfer business, not the wealth creation business.

They are in the business of monetizing their ability to dispense economic privilege to their preferred constituencies, the costs of which are huge & borne by all of us. They extract a variety of personal commissions in currencies that are mostly alien to those in the commercial world (extortions, soft emoluments of political votes or payments for economic privilege, power or other) and create macro costs that are huge & real, but kind of hidden.

The target has always been other peoples’ money, but now the incremental drag on GDP and force of unsustainable leverage has upped the urgency: “I’m out of money. Give me yours.”

The target is other peoples’ money, and it is a target rich environment … your firm's money, your money, your parent’s money, your kids’ money.

Tell them no.

What is your economic outlook?

WWB are not economists, and we generally don’t fare well in any forecasting. But you asked, so … from our perspective, we just locked in a huge cloud of uncertainty across all dimensions of the US economy until well after the 2012 election. That uncertainty will be transmitted to global economies.

Look for nominal growth of 0%<GDP<2%, if not a few quarters of negative numbers. We expect employment will flatline, go sideways to nominally up, but would not be surprised to see that too go negative from time to time. We anticipate corporate capital budgets will be trimmed, limited to only near term high certainty payoffs or strategically important or competitively disruptive initiatives. Emerging markets may continue to attract new capital investments on the margin, but that goes away in a heartbeat if corporations see uncertainty in global demand: “Who shall buy these widgets?” And that likely happened today.

So our takeaway

- Liquidity first, long term investment second. We could be sideways for a while.

- Diversification & risk parameters run the book.

- Now is not a good time to reach for higher expected returns or yield ("never" is a good time to reach for yield)

- If you think you have a good macro bead on what happening, you’re likely wrong.

Look for some more big volatility, perhaps some Europigbanks go boom and get nationalized … again … and then it’s going to get really quiet. Volatility will vanish, but it will be the scary kind of quiet, when absence of volatility indicates fear. People will have their risk books tucked away. Volatility will drop because nothing will be happening.

The Fed’s out of ammo. The banks are out of capital. The government’s broke. The language is false. Prices are unreliable. Things get quiet during a rebuild. Standards of living decline. It’s a grim business, and it's slow.

Where we go from there is the issue.

If you believe that the US will be a market driven economy, equities actually look good if you have staying power. Private investment in wealth creating businesses (non-listed, low/no regulation risk) will be increasingly more attractive IF there is a restoration of rule of law, contract rights, and sensible regulatory costs.

If you believe that the US will devolve more completely into a redistributionist economy, gold, diamonds and portables look good as do opportunities in the black market. The alternative will be to join Jeff Imeldt on the President’s Council on Employment or get a job with the government. FDIC and FINRA will be hiring.

I’d personally not bank on the shovel ready stuff: it might be a while. So the short answer is that we have to wait until the elections for clarity and then probably another year after that to even have a clue.

8/3/11

Update on Saturday, August 6, 2011 at 04:46PM by

hb

hb

Note the date of our posting. The downgrade report of Aug. 5, 2011, by Standard & Poors is here:

United States of America Long-Term Rating Lowered To 'AA+' On Political Risks And Rising Debt Burden; Outlook Negative

Rating Lowered To From

United States of America (Unsolicited Ratings)

Federal Reserve System (Unsolicited Ratings)

Federal Reserve Bank of New York (Unsolicited Ratings)

Sovereign Credit Rating AA+/Negative/A-1+ AAA/Watch Neg/A-1+

It is the responsibility of leadership to solve problems. Part of that responsibility entails bringing attention, forcing attention and resources to solve critical problems. So, if the house is on fire, you call the fire department.

We call for Tim Geithner's resignation.

Update on Monday, August 8, 2011 at 09:18AM by

hb

Standard & Poor’s Clarifies Assumption Used On Discretionary Spending

S&P used the Alternative Fiscal Scenario of the nonpartisan Congressional Budget Office (CBO) and Treasury and the administration are characterizing this as a "mistake". Hmmm... credit judgement or mistake? It would be one thing if Treasury had any credibility. Perhaps S&P was using Turbo Tax?

Here's the fine print on that one:

The Alternative Fiscal Scenario

The budget outlook is much bleaker under the alternative fiscal scenario, which incorporates several changes to current law that are widely expected to occur or that would modify some provisions of law that might be difficult to sustain for a long period. Most important are the assumptions about revenues: that the tax cuts enacted since 2001 and extended most recently in 2010 will be extended; that the reach of the alternative minimum tax will be restrained to stay close to its historical extent; and that over the longer run, tax law will evolve further so that revenues remain near their historical average of 18 percent of GDP. This scenario also incorporates assumptions that Medicare’s payment rates for physicians will remain at current levels (rather than declining by about a third, as under current law) and that some policies enacted in the March 2010 health care legislation to restrain growth in federal health care spending will not continue in effect after 2021. In addition, the alternative scenario includes an assumption that spending on activities other than the major mandatory health care programs, Social Security, and interest on the debt will not fall quite as low as under the extended-baseline scenario, although it will still fall to its lowest level (relative to GDP) since before World War II.